Apr 29, 2026

We are seeing emerging investor consensus that Marketplaces are more likely strengthened than challenged by AI - especially Transactional Marketplaces

Public markets have been in a rush to reprice online platform and marketplace businesses for the AI era.

Already one clear pattern has emerged: investors are not expecting all platform and marketplace business models to be disrupted equally. Some multiples are being compressed aggressively, others are holding up, and a few are even starting to pull away.

As marketplace and platform advisors and dealmakers, our focus here is the market cap evolution of transactional and subscriptions marketplaces. We also find it instructive to compare the performance of marketplaces with that of top SaaS platforms.

What is happening to valuations?

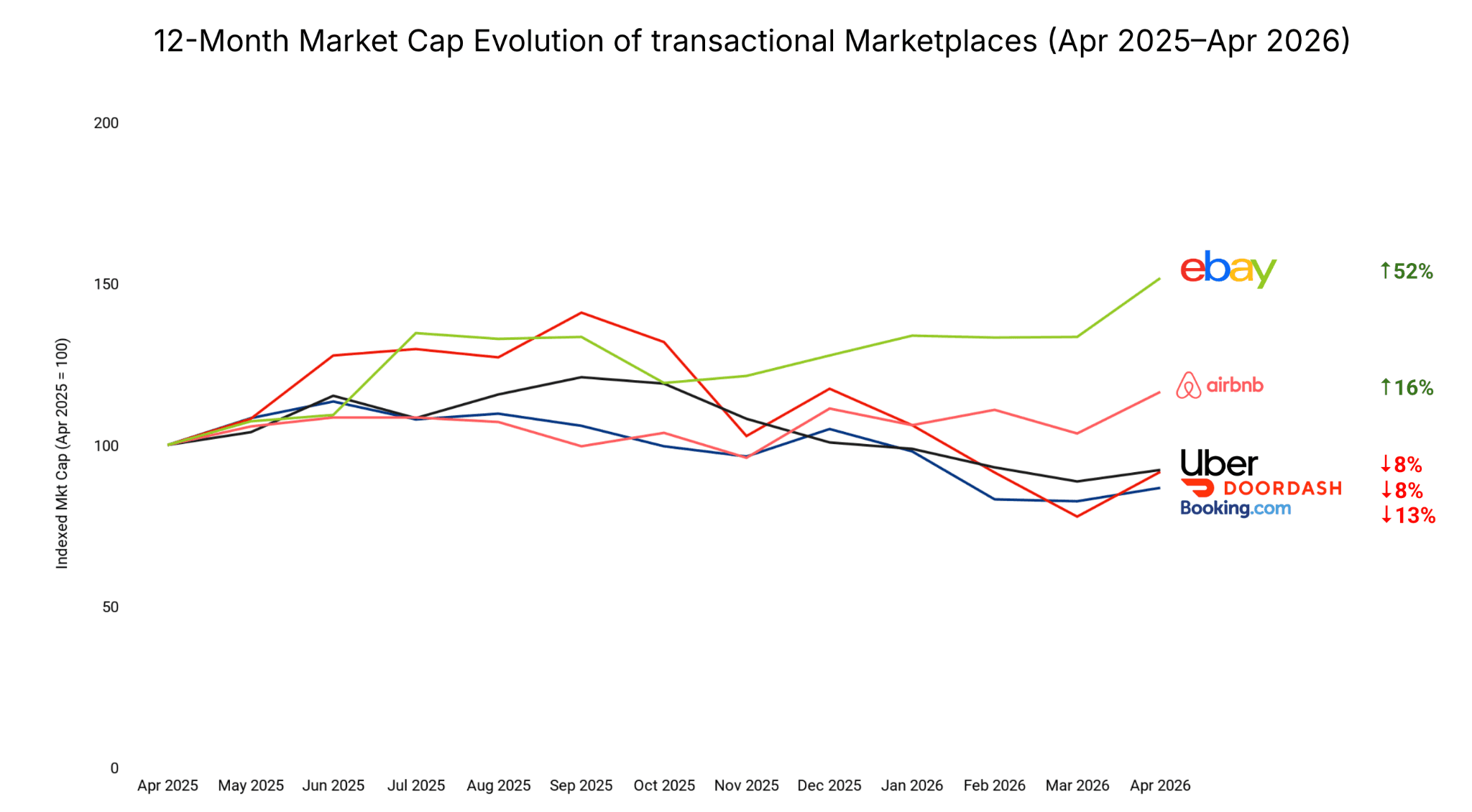

Transactional marketplaces

-13% to +52% over 12 months in our sample.

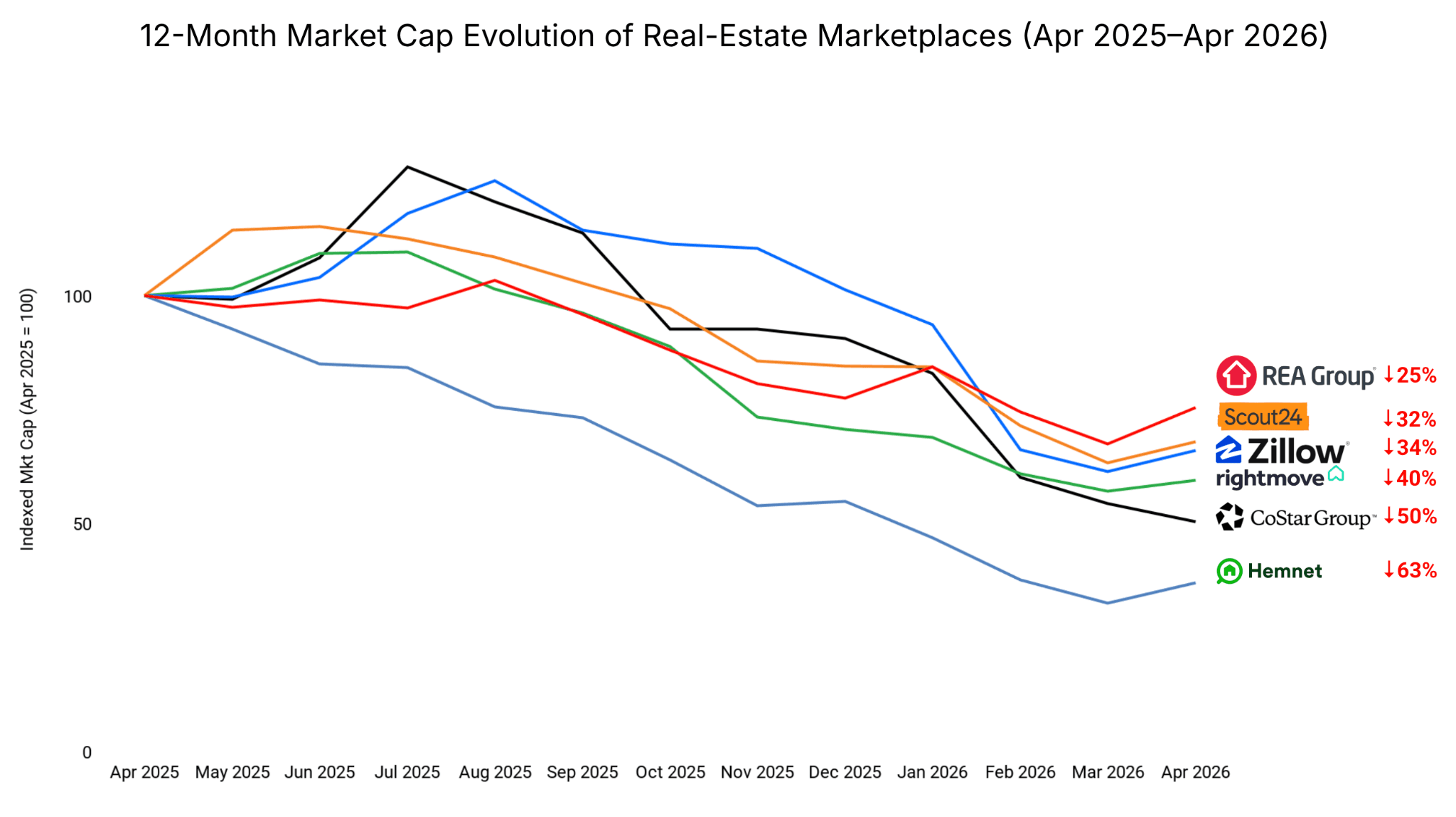

Subscription and classifieds marketplaces

a) Real estate down -25% to -63% over 12 months

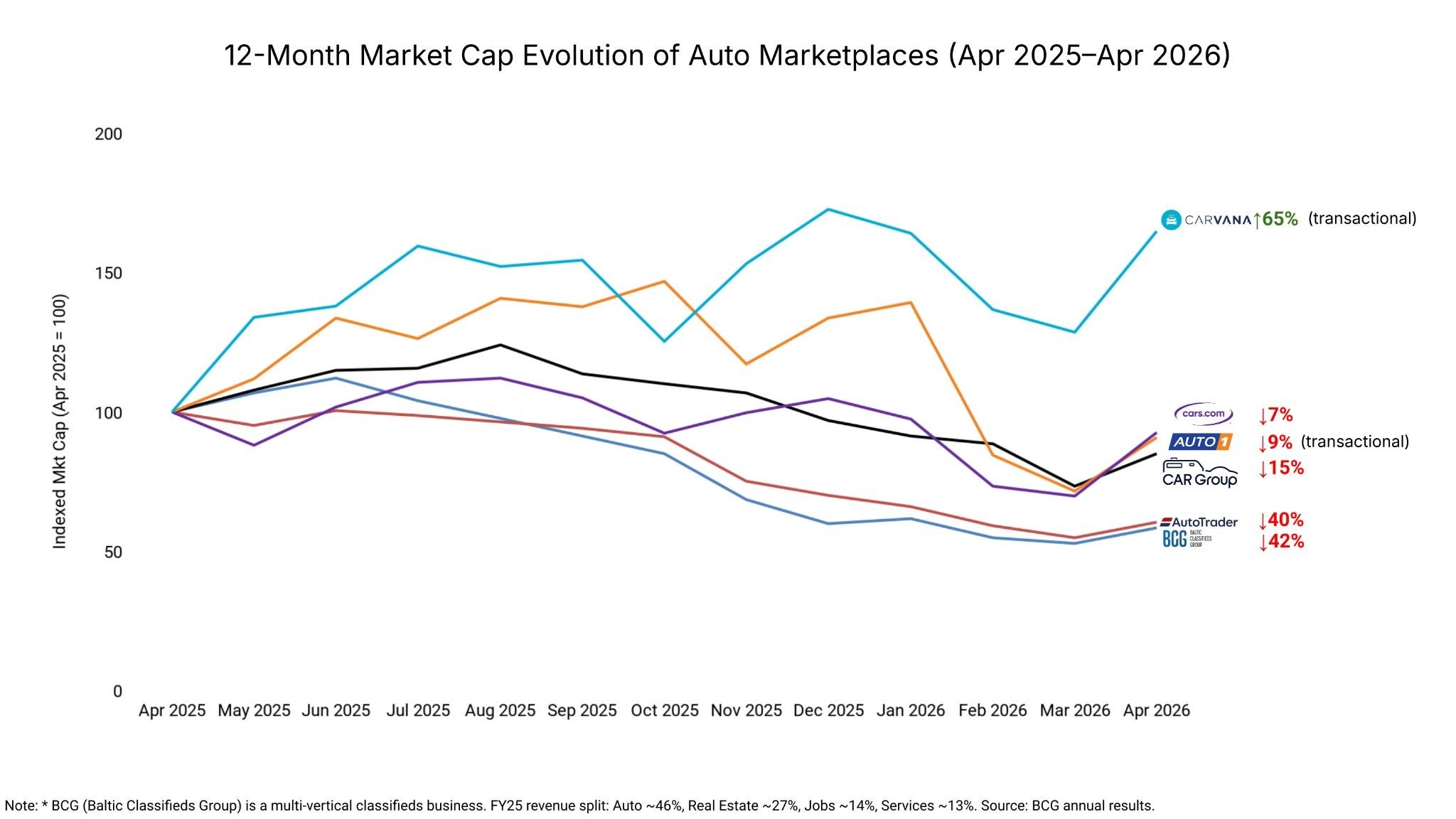

b) Automotive down -7% to -42% for classifieds and -9% to +65% for transactional models

The transactional vs. subscriptions model share price variance over the last 12 months is well illustrated and within the Auto vertical. Carvana (transactional) is up 65%, while Auto1 (also transactional) is down (just) 9%. Carvana owns the full operating stack: inventory, financing, logistics, returns, warranty. Auto1 runs a C2B model that connects consumer sellers to dealer buyers, with less inventory risk; their B2C business accounts for little more than 10% of total sales. The auto classifieds cluster (predominantly subscriptions-based) has moved in the other direction: AutoTrader UK -40%, BCG (a generalist and multi-vertical with 46% automotive revenues) -42%, CAR Group -15%, Cars.com -7%. The within auto sector divergence is the cleanest indicator that the resilience gap is more about business model than industry exposure.

Transactional vs subscription marketplaces.

Both the automotive transactional players (Carvana, Auto1) and the classifieds players benefit from fundamental marketplace strengths. Both have two-sided network effects. Both build trust, brand and proprietary-data moats. So why the diverging share price performance?

Our earlier article on Why property portals are such great businesses (September 2025) made the case that subscription portals such as Rightmove, REA and ImmoScout24 are some of the most defensible digital businesses ever built; that case has not changed. Rightmove still commands roughly 80% of UK property search time. Hemnet still reaches close to 90% of all Swedish property sellers. The structural advantages are intact.

What has changed is how the market is pricing the next chapter. Subscription marketplaces sit higher up the funnel - one step removed from the transaction - the true moment of value creation. They are paid by agents and developers (or car dealers) for delivering buyer leads; the transaction itself happens elsewhere. In an AI-mediated discovery world, that ‘find’ function is exactly the layer LLMs and agents can also play in, even if much of the supply still lives on the portal.

Transactional marketplaces by definition sit where the transaction is happening. Taking the example of Carvana ($89B market cap) - to complete a single transaction, the platform inspects the vehicle, reconditions it, holds title, finances the buyer, dispatches transport, honours a 7-day returns policy, and stands behind warranty claims. Each of these is a capability built and refined over years. It's not something a generalist LLM can add much value to. A similar operating stack runs through Uber ($154B), Booking ($138B), and DoorDash ($77B).

Why might transactional marketplaces be harder for AI to disrupt?

Operational complexity. Transactional marketplaces orchestrate physical and financial flows that generalist LLMs cannot easily disintermediate. Real-time logistics, payments, KYC, fraud screening, dispute resolution, regulatory compliance, supply onboarding. Yes, every step will become faster and cheaper with AI agents, but these we expect to be subordinate to today’s leading platforms, not in competition with them.

Trust. We argued in our piece on Marketplace Moats in the Age of AI (January 2026) that AI agent adoption is likely to be inversely proportional to the level of rational and emotional involvement in the purchase. Low-stakes commodity replenishment delegates well to agents. High-stakes transactions, like buying a flat in Berlin, a used car, or hiring a co-worker, still require trust infrastructure that agents cannot yet provide. Many valuable transactional marketplaces are concentrated in exactly these higher-involvement categories.

The AI feeder effect. Where transactional marketplaces meet the AI agent layer, they are increasingly the destination, not the disintermediated middle. Hotel queries inside ChatGPT are routed to Booking. Etsy is testing embedded checkout inside LLM interfaces. The transaction infrastructure is what the agent calls; the agent does not replace it.

Within the subscription cohort, the picture splits in two.

Property and auto classifieds (Rightmove, ImmoScout24, REA, BCG, AutoTrader UK) have all suffered hard re-ratings, but their underlying revenue keeps growing. Margins remain above 60%, churn is negligible, ARPA still holds/rises. This is multiple compression on solid financials. And this kind of de-rating can reverse - at least in part - under 3 conditions.

Firstly, revenues and EBITDA continue to grow.

Secondly that LLMs become trusted traffic partners to property and car classifieds (as Google has become).

And thirdly, if the same “classifieds” platforms can use AI to take out cost, enhance usability, and get closer to the transaction.

In our view, property and auto portals are being de-rated too hastily on concerns LLMs will hog the top of the funnel at a time when LLM’s rarely deliver even 1% of traffic, and incumbent fundamentals show no signs of decline. What is clear is they will have to adapt. They will as a minimum need to provide conversational interfaces, smarter personalization, recommendations, and further value add to agents and developers, for example by rating lead quality based upon a users’ individual portal behaviour. It is quite likely the subscriptions model will need to make way to a pay-per-qualified lead model (a trend happening faster in recruitment marketplaces where pay per qualified applicant is a necessary response to applicant spam on auto-apply). In property classifieds, there are plenty of examples of PPL monetizing well, and even better than subscriptions models (e.g. PropertyFinder, Bayut in UAE).

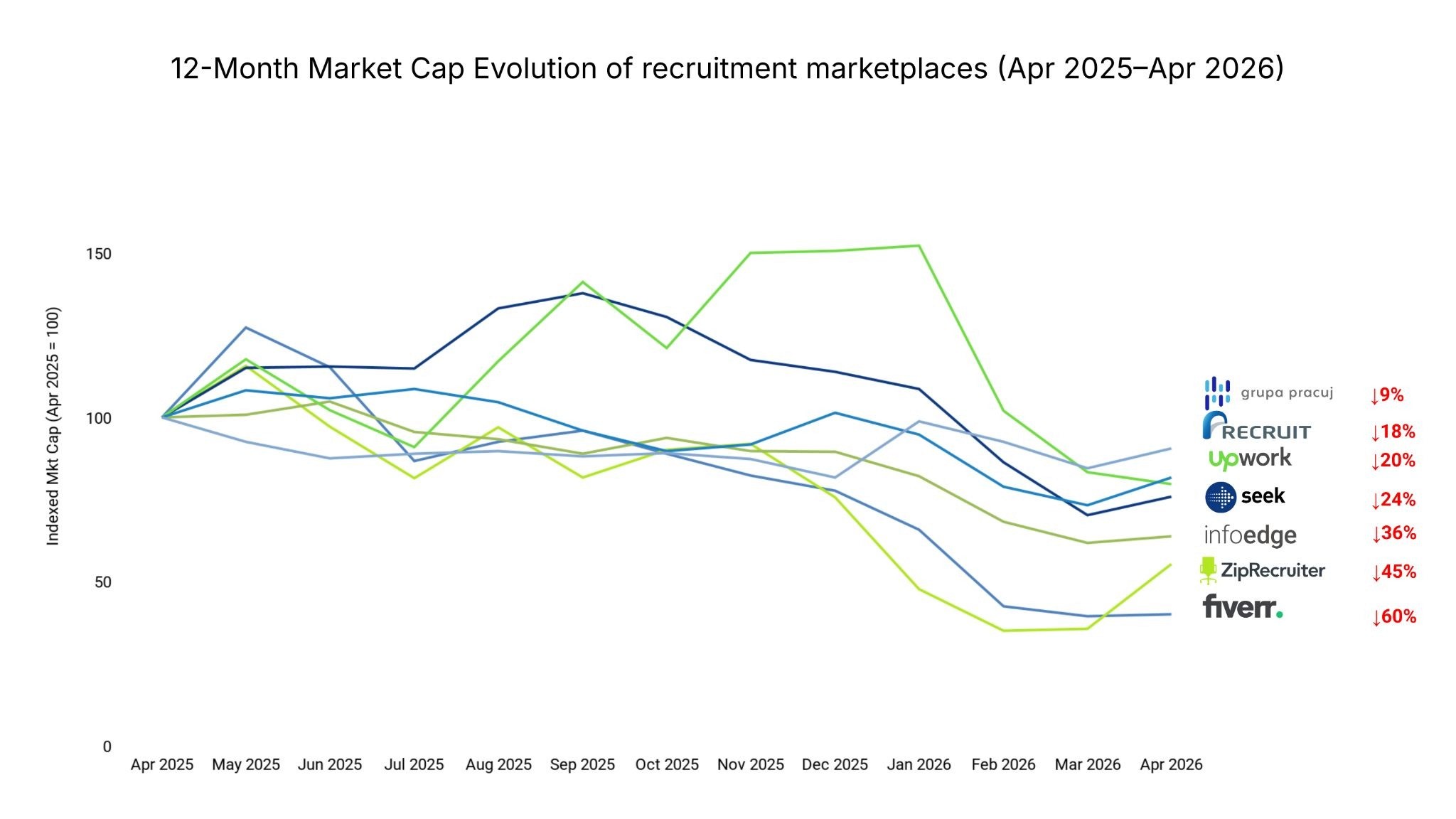

Recruitment classifieds are under more pressure.

Unlike car and real estate classifieds players, wherever they are, recruitment classifieds have to contend with an increasingly AI-enabled LinkedIn and Indeed. In the case of ZipRecruiter, the decline has been brutal. The company listed at a $2.2 billion valuation in 2021. It trades below $250 million today, a near 90% decline. Revenue fell from $905 million in 2022 to $449 million in 2025. When it announced a ChatGPT integration in March 2026, the stock fell further. The market is betting that AI native challengers - including those using LinkedIn and GitHub as their “CV database” are better placed to provide the end-to-end recruitment service employers are increasingly demanding. AI-native challengers like Mercor, Findem, hireEZ and Jack & Jill are likely to pick up that demand.

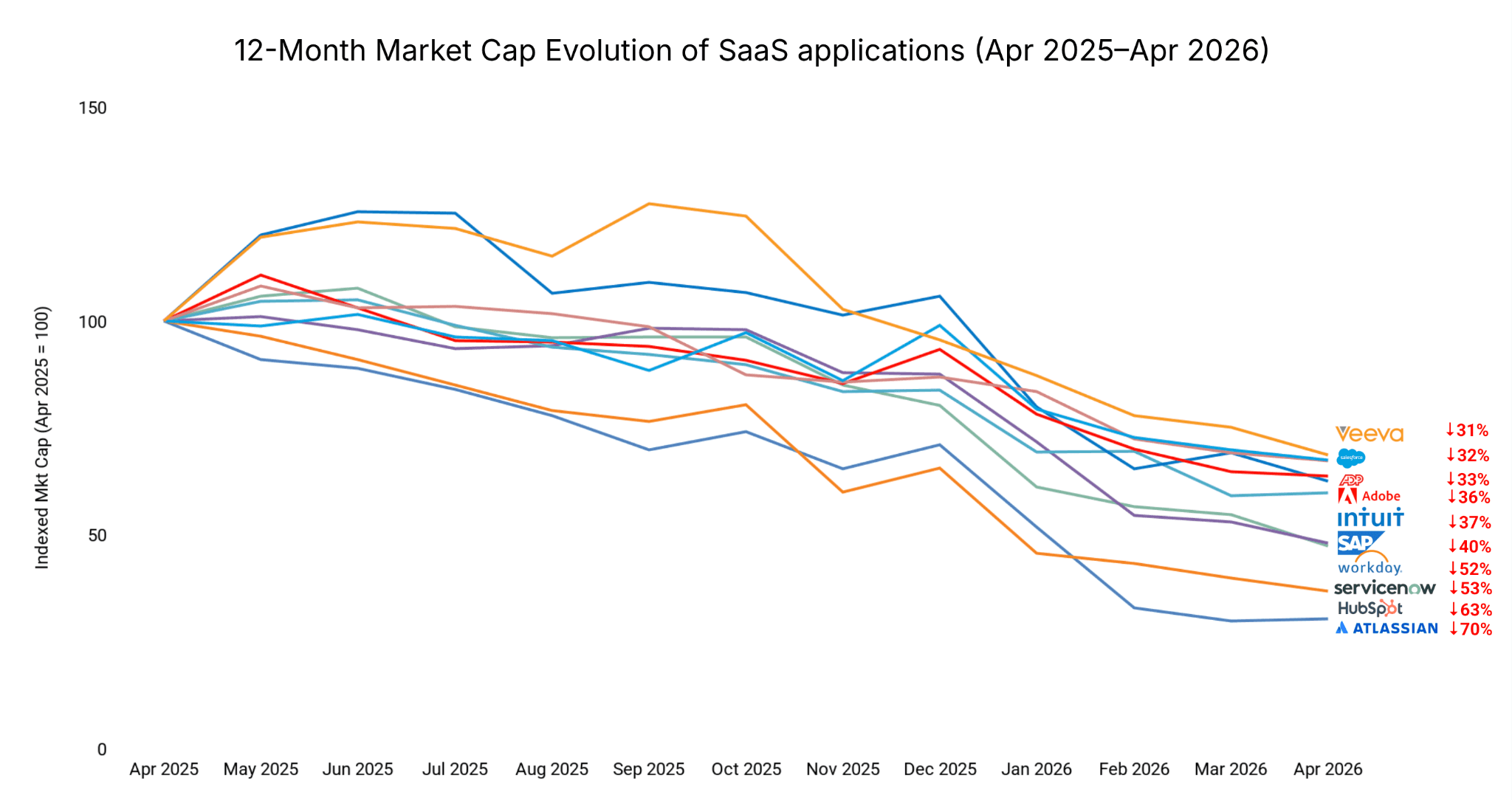

How subscription marketplaces compare with SaaS.

An insightful comparison for subscription marketplaces is application SaaS. Both share the recurring-revenue mechanic that fuelled Venture Capital’s love affair with B2B SaaS over the last decade and a half. Yet over 12 months, application SaaS has been hammered harder than any of the classifieds models.

Application SaaS sells codified workflows, and codified workflows are exactly what LLMs and AI native platforms replicate best. Atlassian (-70%), HubSpot (-63%), ServiceNow (-53%), Workday (-52%), Adobe (-36%), Salesforce (-32%) have all been re-rated as the market starts to price what happens when AI replaces the workflow they sell. Or when coding tools like Replit and Lovable deliver 80% of the value for under 20% of the cost. And simplify the migration from incumbent to challenger platform.

Or just produce a better product.

Even Salesforce, the relative outperformer, is down a third. The customer-record lock-in that defined Salesforce’s defensibility still has some structural value, but even that is being tested.

Conclusion: why marketplaces, remain attractive and all will become “transactional”

The era when stable SaaS multiples underpinned a valuable subscription software sector is over. The public markets are starting to differentiate between business models which look most exposed to AI, and those that by monetizing the transaction itself, in all its complexity, look least exposed to value erosion, and likely beneficiaries of AI. Marketplaces sit firmly on the resilient side of that divide..

Within marketplaces, transactional marketplaces look the most resilient. Property and auto classifieds remain digital fortresses with intact economics that have de-rated on AI uncertainty. Yet most have a roadmap that may well enable them to rerate. Some but not all will succeed. Recruitment classifieds face the largest challenge and will need to become transactional faster, by evolving into end-to-end recruitment platforms.