Jun 4, 2026

What Happened to Early-Stage European Marketplace Investments 2021-25?

Big Picture

EIV has analysed over 1,000 European marketplace funding rounds of <$10M, between 2021 and 2025. We wanted to understand how early stage marketplace funding has changed by volume and value per vertical since their 2021 peak. We discovered a varied landscape with some marketplace verticals seeing their best ever levels of investor interest in 2025. We hope it will prove insightful to early stage marketplace founders and investors alike.

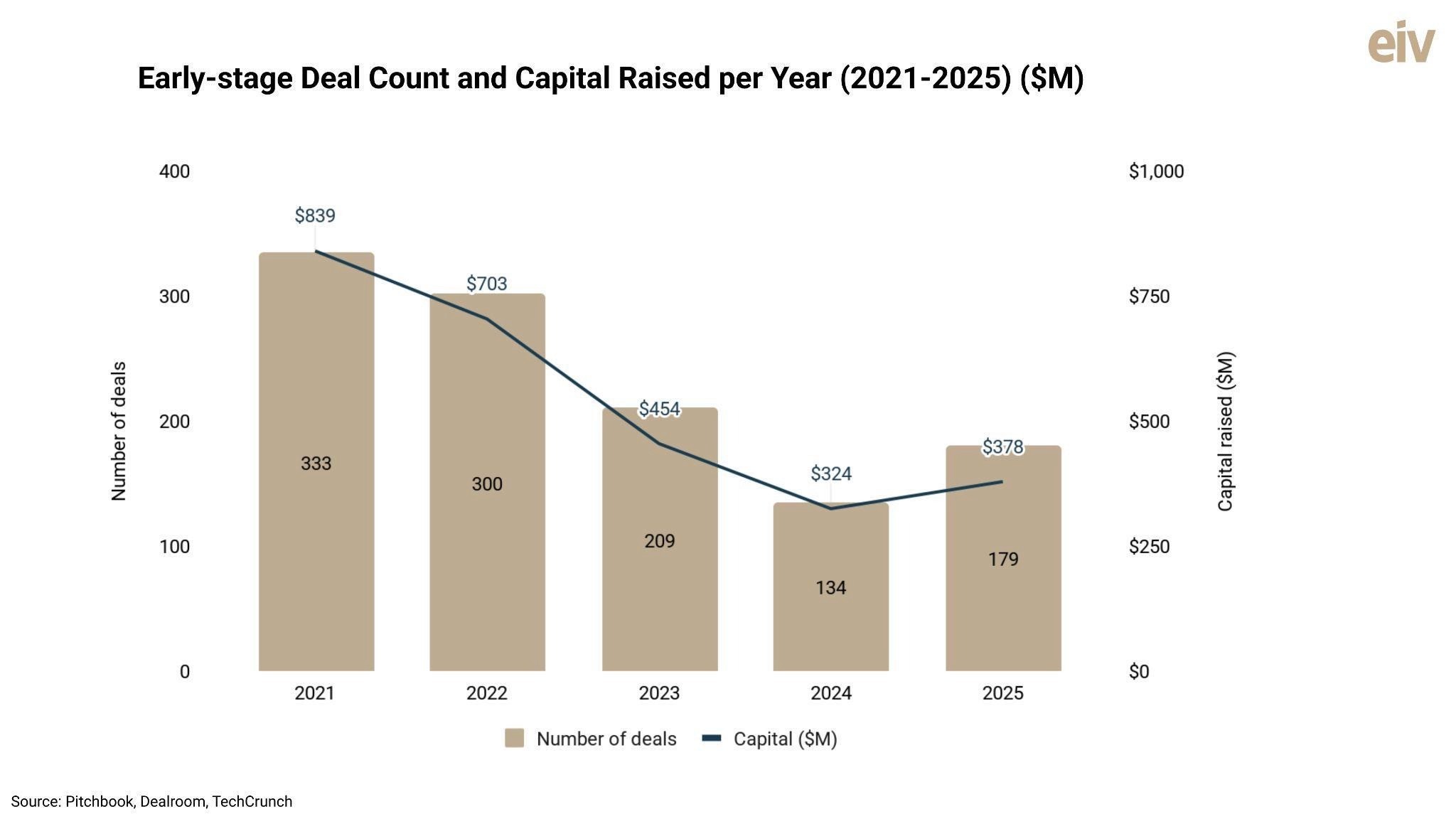

During 2021-25, early stage European marketplaces and platforms raised $2.70B across 1,155 rounds. Capital invested fell from $839M in 2021 to $378M in 2025. Deal volume fell in parallel, from 333 rounds in 2021 to just 179 in 2025.

Per Vertical View

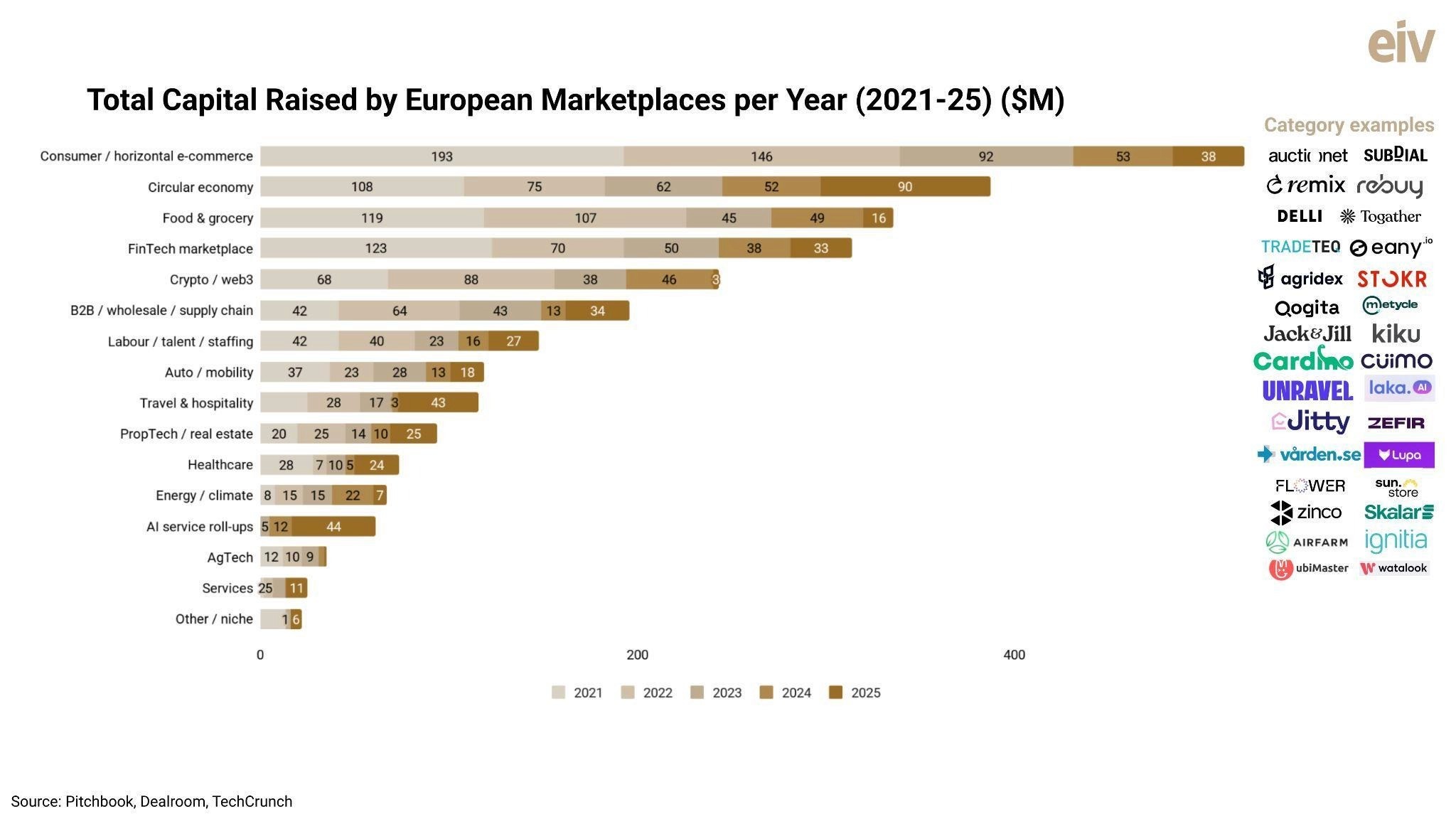

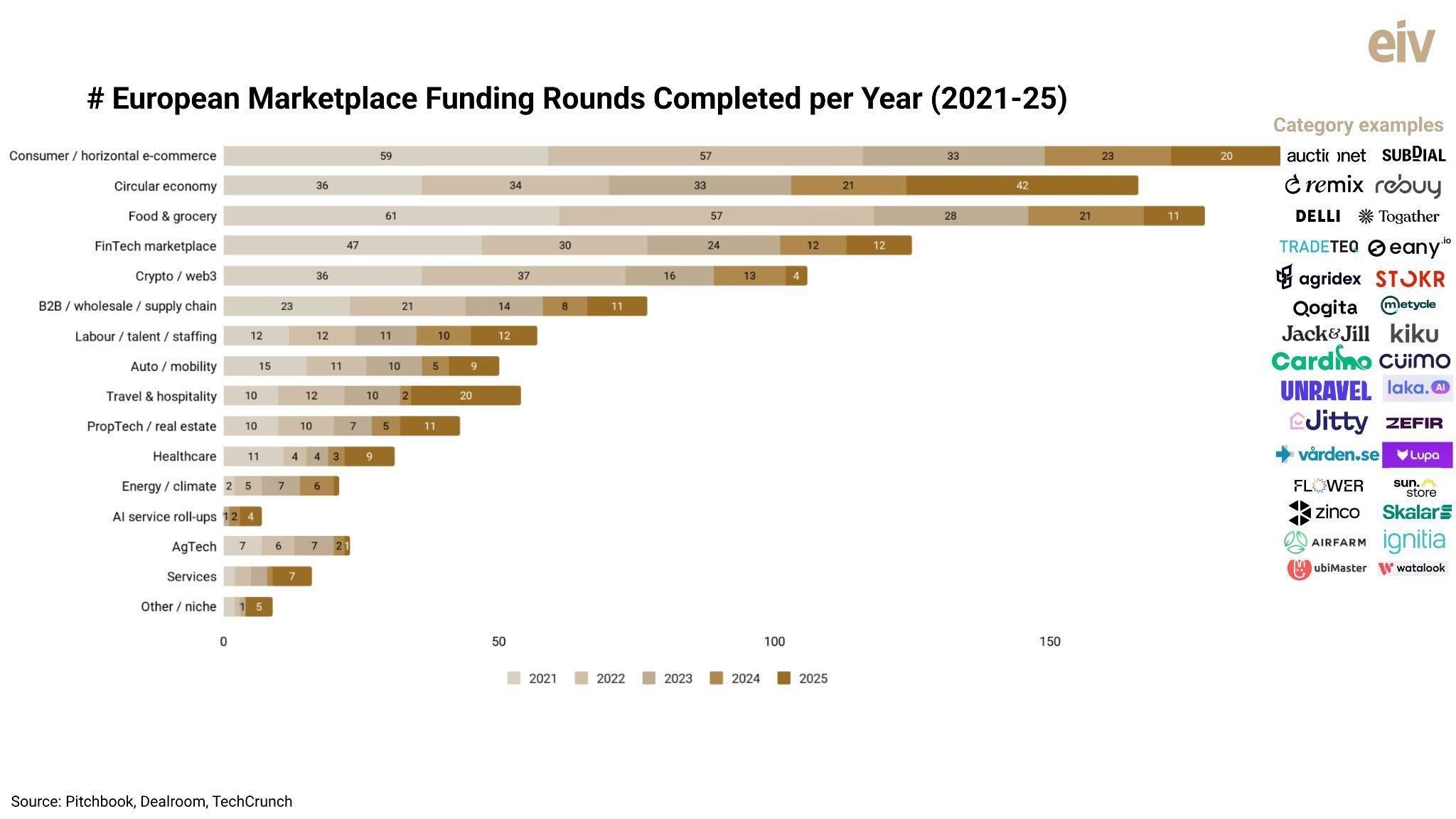

According to our analysis, the 3 marketplace verticals seeing the largest growth in deal volume between 2021and 2025 were:

Circular Economy: Climbed from 36 to 42 deals, with capital raised at $90M (down from $108M in 2021), as buying used, repaired, or recycled goods became mainstream

Travel & Hospitality: Doubled from 10 to 20 deals, with capital rising from $25M to $43M, as global travel surged back from the pandemic and became more specialized

Services: Rose from 2 to 7 deals, with capital growing from $2M to $11M, driven by platforms that digitize local, everyday labor

On the flip side, the top 3 losers experiencing the steepest drops in deal volume 2021-25 were:

Food & Grocery: Plummeted from 61 to just 11 deals, with capital declining from $119M to $16M, as early stage funding for fast delivery apps dried up

Crypto / Web3: Crashed from 36 to just 4 deals, with capital falling from $68M to $3M as a crypto bubble burst

Consumer & Horizontal E-Commerce: Collapsed from 59 to 20 deals with capital dropping from $193M to $38M as funding started moving away from horizontal e-commerce to specialized vertical platforms.

We explore each vertical in a little more detail below:

Consumer & Horizontal E-Commerce

Consumer and horizontal e-commerce experienced a continuous decline in both deal volume and capital deployed between 2021 and 2025, with financings plunging from 59 to 20 and funding dropping from $192.6M to $37.9M. During the peak market activity of 2021 to 2023, investors backed niche consumer marketplaces to capture specific retail categories, including Colizey ($10M, sports equipment marketplace), CGTrader ($10M, 3D asset marketplace), WOW Concept ($9M, curated fashion and lifestyle marketplace), and LoveCrafts ($8M, crafting marketplace). In 2024 and 2025, investor appetite moved to platforms like Wimt ($10M, social commerce marketplace), eBrands ($8M, consumer brand platform), Auctionet ($7M, online auction marketplace), and Subdial ($3M, luxury watch marketplace).

Circular Economy

Circular economy marketplaces have seen deal volume climb from 36 in 2021 to 42 in 2025, and capital falling only slightly from $107.6M to $90.3M. Between 2021 and 2023, early stage capital backed resale and reuse models across fashion, furniture and children's goods, including Sellpy ($10M, second-hand goods marketplace), and Flip ($7M, recommerce marketplace). By 2024 and 2025, funding split between category-specific resale and a resale-as-a-service layer sold to retailers, backing Underdog ($8M, refurbished home appliance marketplace), Brandback ($7M, branded resale platform), Remix ($5M, second-hand consigned fashion) and Alpagga ($6M, used industrial equipment). The category's ability to consistently produce venture-backed entrants throughout the funding cycle, suggests investors increasingly view circular consumption as a broad behavioural shift with considerable scope to evolve further.

Food & Grocery

Food and grocery funding saw a severe downward correction from its 2021 peak of 61 deals and $119.1M to close 2025 with just 11 deals and $15.7M. During the 2021–2023 convenience boom, capital targeted broad consumer delivery, event catering, and localized distribution setups like Togather ($8M, event catering marketplace), Slerp ($7M, direct-to-consumer ordering platform), and Delli ($7M, independent food producer marketplace). In 2024 and 2025 a severe correction ensued, where broad, fleet-dependent delivery models lost out in favor of niche networks rooted in local food provenance and bespoke logistics, such as L'Orto Di Jack ($4M, local produce marketplace) and Forno Brisa ($3M, artisan food marketplace).

FinTech Marketplaces

FinTech marketplace funding shrank from its 2021 peak of 47 deals and $122.9M to close 2025 with just 12 deals and $33.4M. Between 2021 and 2023, initial capital flows targeted trade finance and private asset matching platforms, backing networks like STEP ($10M, digital wealth marketplace), Tradeteq ($10M, trade finance marketplace), and Mitigram ($7M, trade finance marketplace). In 2024 and 2025, investors doubled down on institutional alternative assets and private market transactions, backing platforms like Primary Portal ($10M, private market securities marketplace), Wealthcome ($7M, wealth management marketplace), and DealCircle ($6M, M&A marketplace).

Crypto & Web3

Crypto and Web3 marketplace funding traced a classic bubble-and-correction arc, suffering an intense structural drop from its 2021 peak of 36 deals and $68.2M to close 2025 with just 4 deals and $3.3M. In the peak liquidity stretch of 2021 to 2023, financing flocked to digital assets, creator storefronts, and gaming ecosystems, anchoring rounds for Vulcan Forged ($8M, blockchain gaming marketplace), Starly ($6M, NFT marketplace), and Atlas DEX ($6M, decentralised exchange). Conversely, the 2024 and 2025 phase abandoned consumer NFT concepts, with remaining capital going into real-world asset security tokenization and institutional trading layers like Agridex International ($9M, tokenization and exchange of crops etc.) and STOKR ($8M, digital securities marketplace).

B2B, Wholesale & Supply Chain

B2B supply chain marketplace funding has proven resilient, managing a minimal contraction from its 2021 level of 23 deals and $42.4M to close 2025 with 11 deals and $34.4M raised. From 2021 to 2023, funding concentrated on digitizing traditionally fragmented merchant procurement layers, yielding notable early rounds for Qogita ($10M, wholesale goods marketplace), Vamstar ($9M, healthcare procurement marketplace), and Koltiva ($8M, agricultural supply-chain marketplace). Over 2024 and 2025, the investment thesis evolved to managing complex manufacturing processes and integrated industrial logistics, driving capital into automated supply networks like Muvn ($9M, logistics marketplace) and AgrigateOne ($7M, agricultural supply-chain marketplace).

Jobs, Talent & Staffing

Jobs, Talent & Staffing demonstrated consistent deal velocity, maintaining a flat volume path from its 2021 baseline of 12 deals and $42.2M to close 2025 also at 12 deals but only $27M. Throughout 2021-2023, investors poured money into basic matching engines and freelance contractor marketplaces such as Collective ($9M, freelancer services marketplace), Napta ($9M, workforce planning platform), and Newsflare ($7M, user-generated content marketplace). In 2024 and 2025, we observed talent capital shifting toward deep automation and the rise of AI-native recruitment marketplaces, such as Jack & Jill AI ($20M, AI-native recruiting marketplace), Vizzy ($5M, AI-powered recruitment platform), Workfully ($5M, remote talent marketplace), and Kiku ($5M, AI-powered workforce platform).

Auto & Mobility

Auto and mobility funding declined from its 2021 peak of 15 deals and $36.8M to close 2025 with 9 deals and $18.4M. Between 2021 and 2023, funding chased alternative vehicle subscriptions, peer sharing, and dealership infrastructure plays, led by 2trde ($8M, dealer auction marketplace), Faaren Group ($7M, vehicle subscription platform), FlexClub ($5M, vehicle subscription marketplace), and CarJager ($6M, classic car marketplace). In 2024 and 2025, investors favoured platforms addressing specific vehicle types and supply chain solutions like Cüimo ($9M, used motorcycle marketplace), Cardino ($4M, used EV marketplace), and Aampere ($2M, EV sourcing platform).

Travel & Hospitality

Travel and hospitality marketplace funding rose from 10 deals in 2021 and $24.6M to close 2025 with 20 deals and $43.3M raised. From 2021 to 2023, capital supported traditional consumer booking tools and specialized niche tourism setups, including Homefans ($7M, sports travel marketplace), Brigad ($6M, hospitality staffing marketplace), and Borrow A Boat ($4M, boat rental marketplace). After just 2 deals in 2024, the sector bounced back in 2025, replacing conventional booking engines with complex, AI-driven trip discovery networks like Unravel ($7M, AI-powered travel planning marketplace).

PropTech & Real Estate

PropTech and real estate marketplaces remained steady, with deal volume increasing from 10 to 11 and yearly funding rising from $20.3M to $25.2M over the cycle. Over the 2021–2023 timeframe, investments included digitizing asset discovery and rental search models, transaction platforms like Zefir ($5M, home-selling platform), and specialist sites Addland ($5M, land marketplace), and Seniovo ($4M, home renovation marketplace). By 2024/2025, investors were targeting specific friction points inside the property transaction itself, funding integrated transaction, financing, and co-ownership mechanisms like Prosperty Solutions ($6M, digital property transaction platform), Hybr ($4M shared accommodation marketplace) and Jitty ($4M AI-native property search).

Emerging Niche Verticals: Healthcare, AgTech, Services & AI Roll-ups

Beyond the core categories, a set of emerging marketplace verticals have gained traction and point to where new models are forming.

Healthcare slid from 11 deals and $28.0M in 2021 to 9 deals and $24.1M in 2025, expanding from providers into wellness, beauty and pet care, backing Vården.se ($6M, healthcare provider marketplace), Lupa Pets ($4M, veterinary marketplace), Apotekamo ($3M, online pharmacy) and sheerME ($3M, wellness marketplace).

Energy and climate marketplaces remained small throughout, moving from 2 deals and $8.2M in 2021 to 1 deal and $7.0M in 2025, after peaking mid-cycle at 6 deals and $21.6M in 2024. From 2021 to 2023, capital chased distributed energy assets and environmental measurement, backing Flower Infrastructure ($9M, grid flexibility marketplace), Piclo ($6M, energy flexibility marketplace) and OakTree Power ($4M, distributed energy marketplace). In 2024 and 2025, funding concentrated on decarbonisation and procurement, supporting Sun.Store ($7M, solar energy marketplace), Dcycle ($6M, sustainability data marketplace) and Bohr Energie ($4M, renewable energy marketplace).

AgTech declined from 7 deals and $11.6M in 2021 to just 1 deal and $1.4M in 2025, focused throughout on digitising agricultural supply chains, with Ignitia ($4M, agricultural intelligence platform), Airfarm ($3M, agricultural marketplace) and BX Technologies ($3M, livestock marketplace).

Services grew from 2 deals and $1.8M in 2021 to 7 deals and $11.3M in 2025, digitising fragmented professional and consumer work, including ubiMaster ($8M, tutoring marketplace), Sourcerie ($3M, sourcing marketplace) and Watalook ($2M, beauty services marketplace).

AI service roll-ups are the newest model. Seven early-stage financings worth about $61M appeared between 2023 and 2025: Arbio's pre-seed in 2023, Lawhive and Dwelly’s first round in 2024, and Numeris, Integral, Skalar and Zinco in 2025. Many moved rapidly on to raise large growth rounds (which we will cover next time). These are more platform than marketplace, with operators buying fragmented local service businesses, in property management, accounting, legal and primary care, and migrating their core to a common, AI-native operating layer. Whereas the marketplace typically takes a fee for the match, the roll-up buys the supply and keeps the margin.

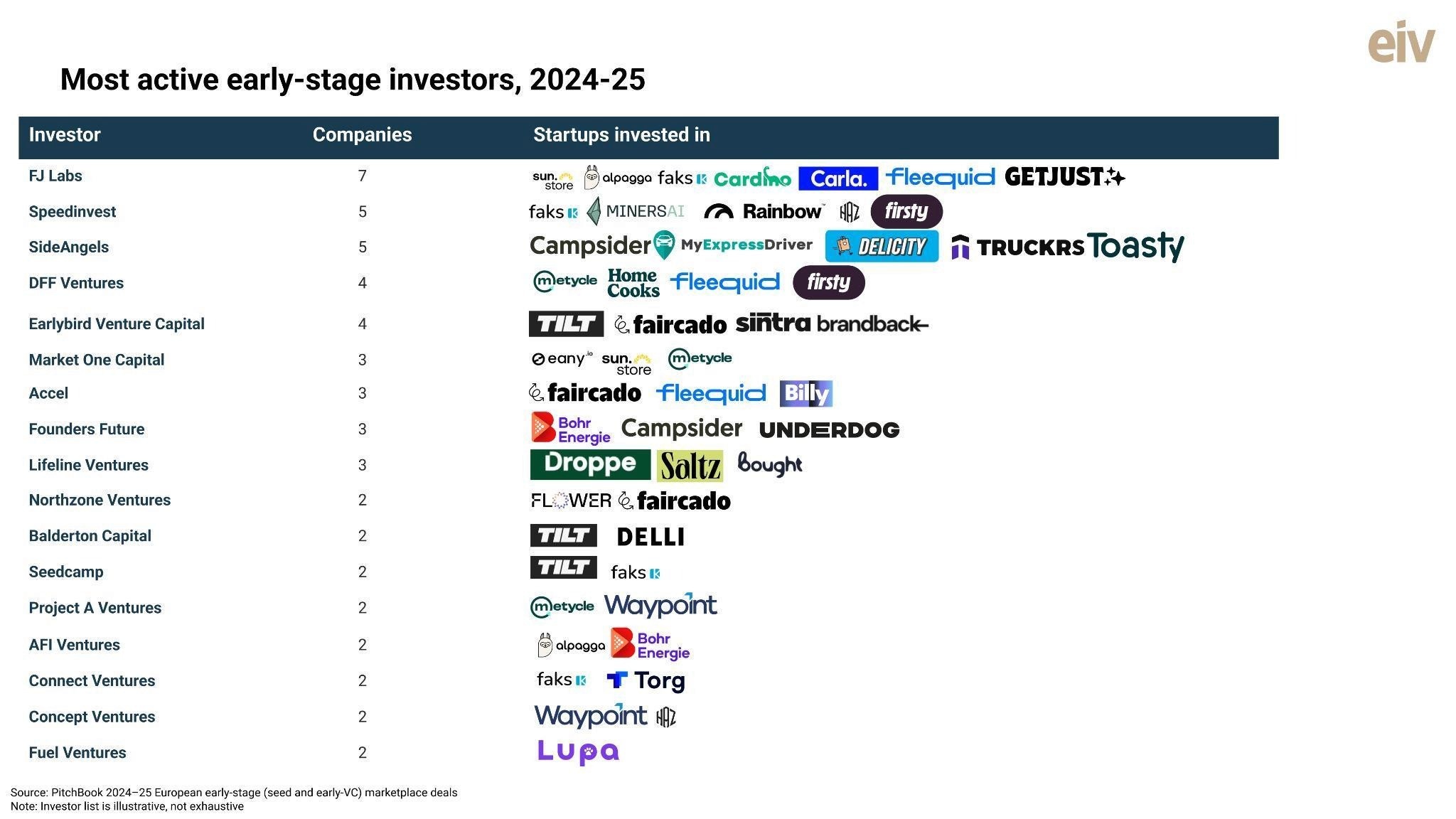

Who are the most active marketplace investors?

There is a small group of serial marketplace investors. New York-based FJ Labs is the most active by far, having funded hundreds of marketplaces for well over a decade, from used EVs (Cardino and Carla) to pharmacy supply (Faks), to used professional kitchen equipment (Alpagga). Market One Capital in Warsaw also runs a marketplace and network-effects thesis, albeit on a much smaller scale; Sun.Store and eany.io are amongst their investments. Around them sit the generalist European early stage funds, Accel, Balderton, Earlybird, HV Capital, Kima Ventures, Northzone, Project A and Speedinvest, to name just a few, that frequently back marketplaces. High-volume seed players like SFC Capital and angel syndicates like SideAngels complete the list of early stage, serial marketplace investors. Their recent picks track many of the trends we have covered here. The fresh money is moving to circular and resale infrastructure, with Faircado, Brandback and METYCLE recurring across their portfolios, and to AI-native models in hiring and local services.

For founders of early stage marketplaces, our advice is also to go beyond the serial marketplace investors and connect with some of the many tens of one-time marketplace investors, who now might well be open to taking a second shot at the space. Unlike many SaaS businesses, many marketplaces are seeing AI deepen their moats while making other marketplaces more profitable. As marketplace advisors, we can also help with investor approaches, especially if your business is already at Series A or beyond.

In our next article we assess how growth and late-stage marketplace investment has evolved over the same period, and identify the key later-stage investors in this space.