Jul 10, 2026

The Marketplace Blueprint: Decades of stellar returns and what drives them

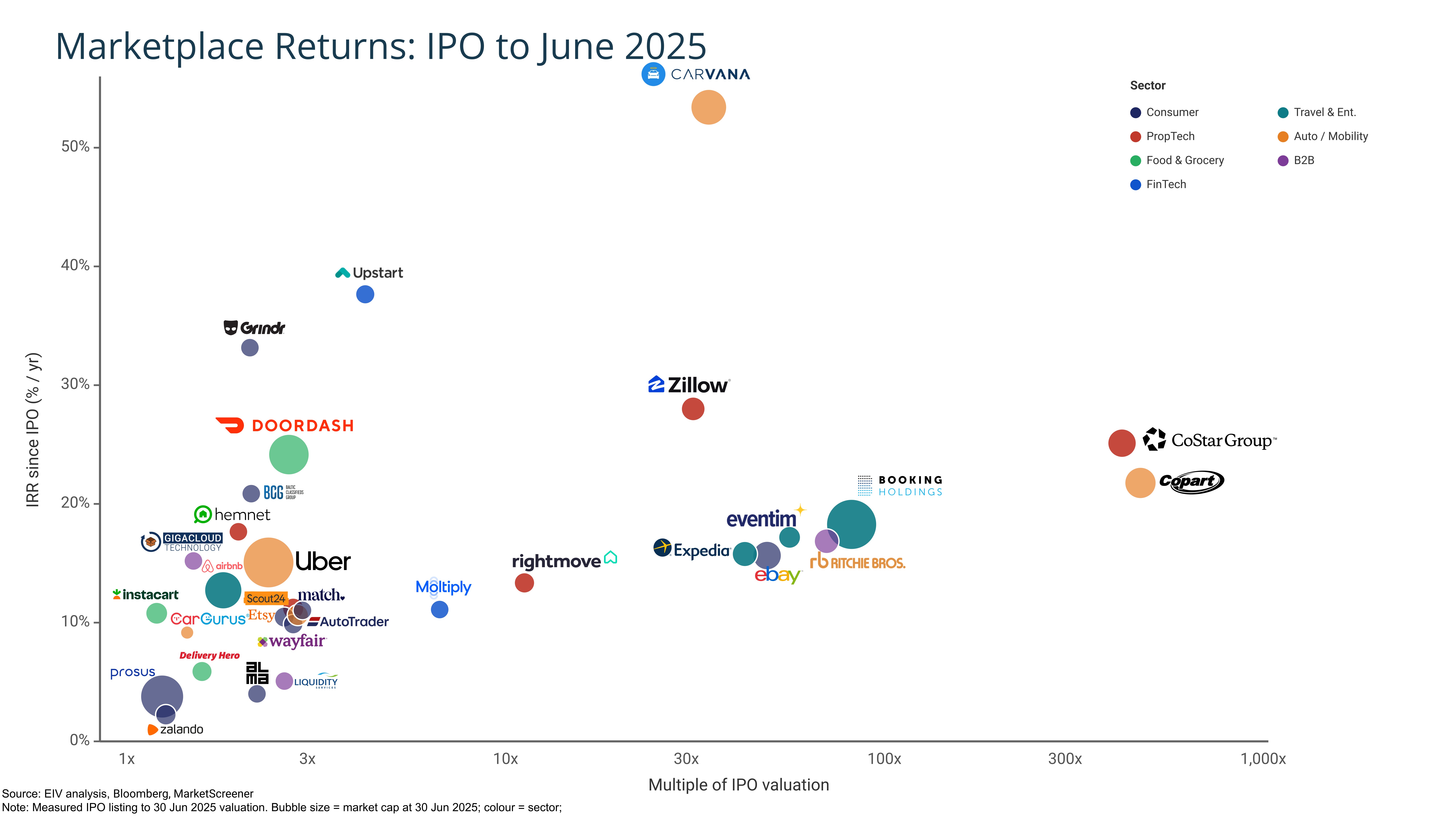

Listed marketplaces were generating value for investors even before Amazon’s IPO in 1997. We analysed the top 90 marketplaces by market cap listed on the US and European exchanges, and measured returns from IPO until today. $590B of IPO value had become $1,430 billion by June 2025 - an XIRR of 13.4%. Adding Amazon raises the June 2025 combined market cap to $3,760B and the XIRR to 23.2%.

In this article we highlight some of the best and worst performers per sector, and share a few perspectives on what has driven their success. Next week, we will review what has happened to some of these companies' valuations over the past 12 months, and ask where today’s valuations seem justified and where maybe less so.

Three of the best performers since IPO are to be found in the US automotive / heavy equipment space:

Used car marketplace Copart has grown 319x in value since its 1994 listing, returning investors 19.5% annually over three decades.

Carvana, the best-performing marketplace of the past decade in any vertical, has delivered 47% a year since 2017 to achieve a 35x return.

RB Global (formerly Ritchie Bros.) has delivered 75x since its 1998 IPO, or 16.5% a year for 27 years

Booking Holdings has scaled a phenomenal 58x since 1999.

Consumer Marketplaces

Consumer is the biggest group in the dataset, returning roughly 28% a year on a dollar invested at IPO. The outsized returns accrued to platforms that owned unique inventory, habitual user demand, or fulfilment infrastructure that could not easily be replicated elsewhere (Amazon, eBay, Etsy, Wayfair).

eBay is valued at 69x their 1998 IPO level - that’s 16% a year for ~28years. Their dominance in collectibles, and unparalleled brand power for pre-owned items, seems more valuable than ever in 2026.

Etsy has returned 3.9x since its 2015 IPO, about 13% a year, to reach $7B. Etsy has built a unique supply of handmade and vintage inventory that exists nowhere else.

Prosus has doubled since its 2019 Amsterdam listing at ~$100B, with most of the gain arriving in the past year (+65%, to $204B). Prosus has become much more than a Tencent tracker, with food delivery and AI-first classifieds (OLX) driving EBITDA growth.

On the negative side, SMG has lost 50% of its September 2025 IPO value. The company owns the top automotive, real estate and generalist classifieds businesses in one of the world’s wealthiest countries - businesses which continue to over deliver.

Travel & Hospitality

Travel marketplaces have delivered returns of about 14% a year.

US-listed Booking Holdings, stemming from the $2.3bn IPO of Priceline in 1999, has generated a 58x return, roughly 16% a year for 27 years, on the deepest hotel-supply network in travel. Returns were 82x as recently as June 2025; it has lost 30% since, despite continued earnings beats, as markets question how much of its search-bought demand survives the shift to LLMs and AI assistants.

Expedia has grown 61x since its 1999 spin-out of Microsoft (~17% a year). It doubled down on B2B supply, growing at double-digits for 18 straight quarters and powering the travel products of banks, airlines and Uber — it has added 42% in the past year.

Airbnb has grown 1.8x since its December 2020 IPO and was one of the few large travel names to hold its value through the past year: its demand arrives directly through its own app, and its supply is largely exclusive.

TripAdvisor, on the other hand, is now worth just a third of its 2011 spin-off value of $1.3bn.

The network effect of having the most travel review content is now under threat from personalized, LLM-generated recommendations.

Food & Grocery

Food delivery generated about 20% a year from IPO until June 2025, easing to about 14% since. The core category thesis for food delivery rewards absolute scale winners (Delivery Hero, Just Eat), while sub-scale regional players face consolidation or exit.

Delivery Hero has returned 2.7x since its 2017 Frankfurt IPO, about 12% a year — most of it restored by the past year's 71% surge, when it became a takeover target.

Just Eat (3.2x from listing to its 2020 acquisition) and Grubhub (3.7x to its 2021 exit) also generated meaningful returns in this sector.

Automotive & Mobility

Autos combined delivered an XIRR of 14% a year from IPO through June 2025.

Carvana has grown 35x since 2017, 47% a year, and the best XIRR in our dataset. Despite a rollercoaster ride in 2022/3, Carvana is increasingly being viewed as a deeply entrenched platform with a structurally more profitable business model than any of its US peers.

Copart has grown 319x since its 1994 IPO, close to 20% a year for three decades. It stood at 474x in June 2025, before its first genuine volume dip took a third off the price. The largest US car auctions platform, matching institutional sellers (leasing, fleet, rental) with consumer and pro buyers, enjoys superlative network effects.

B2B Marketplaces

B2B returned about 14% a year from IPO through today. The vertical delivered the strongest returns where transactions sit inside operational workflows, especially in categories involving physical assets, procurement complexity or proprietary transaction data.

RB Global is the leader of this group, growing their heavy-equipment auctions business 75x since listing as Ritchie Bros in 1998 — about 16.5% a year for 28 years. RB Global is the undisputed leader of a global, transactional marketplace operating across a massive B2B vertical.

Recruitment

Most recruitment marketplaces are trading below their listing prices. The difficulty of building exclusive supply and network effects, combined with the 2 global players LinkedIn and Indeed, has made the lead gen model precarious in most markets for many years. Were it a standalone company today, Indeed would of course be the stand out exception; it is the main factor behind the decline in market values of European and US recruitment marketplaces.

ZipRecruiter — down 87% from its 2021 listing — has now posted four consecutive years of falling revenue, from $905M to $449M.

Grupa Pracuj IPOed in December 2021 at the peak of the global hiring cycle, and was 7.7% down as of June 2026.

PropTech & Real Estate

Proptech marketplaces have grown at about 19% a year from IPO through to June 2025 (but only 13% to June 2026). The last 12 months have seen a dramatic rerating of property portals, which we will have more to say about next week.

Zillow IPOed in 2011 and by June 2025 has delivered annualized returns of 28%, despite writing off its ill-fated iBuying experiment in 2021. Few portals have invested as much as Zillow in re-imagining themselves for an AI-first world. Their share price has nevertheless fallen 50% in the past year.

CoStar has delivered investors 424x from its 1998 listing until June 2025. A two-thirds fall in the last year has lowered these returns to a still impressive 154x (20% per year for 27 years). Investors are concerned that a) CoStar’s core professional data business will be devalued by AI, while b) their recent bets on number 2 / 3 residential portals might not deliver a return. We think investors are only 50% right.

Rightmove, the highly successful UK property portal, had returned 11x between 2006 and June 2025, plus 20 years of dividends. Unprecedented legal action by real estate agents, combined with broader concerns on how AI might squeeze portal revenues have almost halved returns as of June 2026.

Circular Economy

Circular economy marketplaces, including 1stDibs, ThredUp and The RealReal, all have suffered prolonged periods of investor skepticism following stellar IPOs (2021, 2021, 2019 respectively). They are now showing average annual returns of -7% from IPO. Improving unit economics and reaching adjusted EBITDA positive, are beginning to change investor perspectives on these consignment-based models.

The RealReal listed in 2019 at $1.7bn, but collapsed to roughly $100M by 2023 under the belief that luxury fashion consignment was structurally unprofitable. The company has since recovered 15x to $1.5bn after posting positive adjusted EBITDA and restructuring their debt.

There is a deep bench of circular economy marketplaces in Europe that are already profitable or close to it, and are likely to IPO over the next few years - Vinted is the stand out example. Others include Vestiare Collective and Back Market. We expect circular economy IRRs to look very different 5 years from now.

So What does this all mean?

Our key takeaway reiterates the obvious: the best marketplaces have delivered stellar returns for decades. The winning formula tends to combine deep supply penetration with high liquidity. Unique and individual inventory, such as on eBay, AirBnB or Copart, creates further stickiness and loyalty. We are seeing lead gen models - in reviews, price comparison and classifieds come under particular pressure. Some companies in these segments will suffer permanent value impairment, while those that can adapt to an AI-first mindset, are likely to uncover new sources of revenue that potentially drive more value than the lead gen model ever did.

Next week we will take a closer look at which marketplace models have been punished the most by the public markets, and explore which listed marketplaces are most likely to bounce back, based upon strong fundamentals and AI-fuelled innovation.