Mar 26, 2026

Recruitment platforms in the age of AI

Recruitment has been one of the most valuable categories for online marketplaces. For well over a decade, job boards captured that value by bringing direct, SEO, and aggregated traffic, and monetising access to candidates, initially via subscriptions and later on a performance basis.

The model is now under extreme pressure.

A Brief Moment of Nostalgia

Looking back, the 2010’s were the golden era for job boards. Job boards expanded geographically, aggregating audiences, building employer and candidate databases, generating real cashflows. Stepstone acquired UK job boards Totaljobs (2012) and Jobsite (2014), before a KKR-backed consortium in turn bought them in 2020. ANZ’s SEEK consolidated Southeast Asia with acquisitions including JobsDB (2011), JobStreet (2014), and forayed into China with Zhaopin (2014/17).

The two biggest bets in the recruitment space have done well:

In 2012, Recruit Holdings paid approximately $1 billion for Indeed, a platform that had been profitable since 2007, served 80 million monthly visitors across 50 countries, and was growing fast. The multiple: 6.6x revenue, 40x EBITDA. In 2025 Recruit’s HR Tech Division, in which Indeed plays the star role, generated $7.4B in revenue and ~$2.5B EBITDA.

Four years later, Microsoft paid $26.2 billion for LinkedIn, a 50% premium to the market price at the time, and roughly 9x revenue (~$3 billion in 2015). In 2025, LinkedIn generated ~$17.8 billion in revenue, of which we estimate ~$8 billion came from recruitment services (assuming ~45% of revenue, down from ~60–70% historically).

Why the 2020s look different

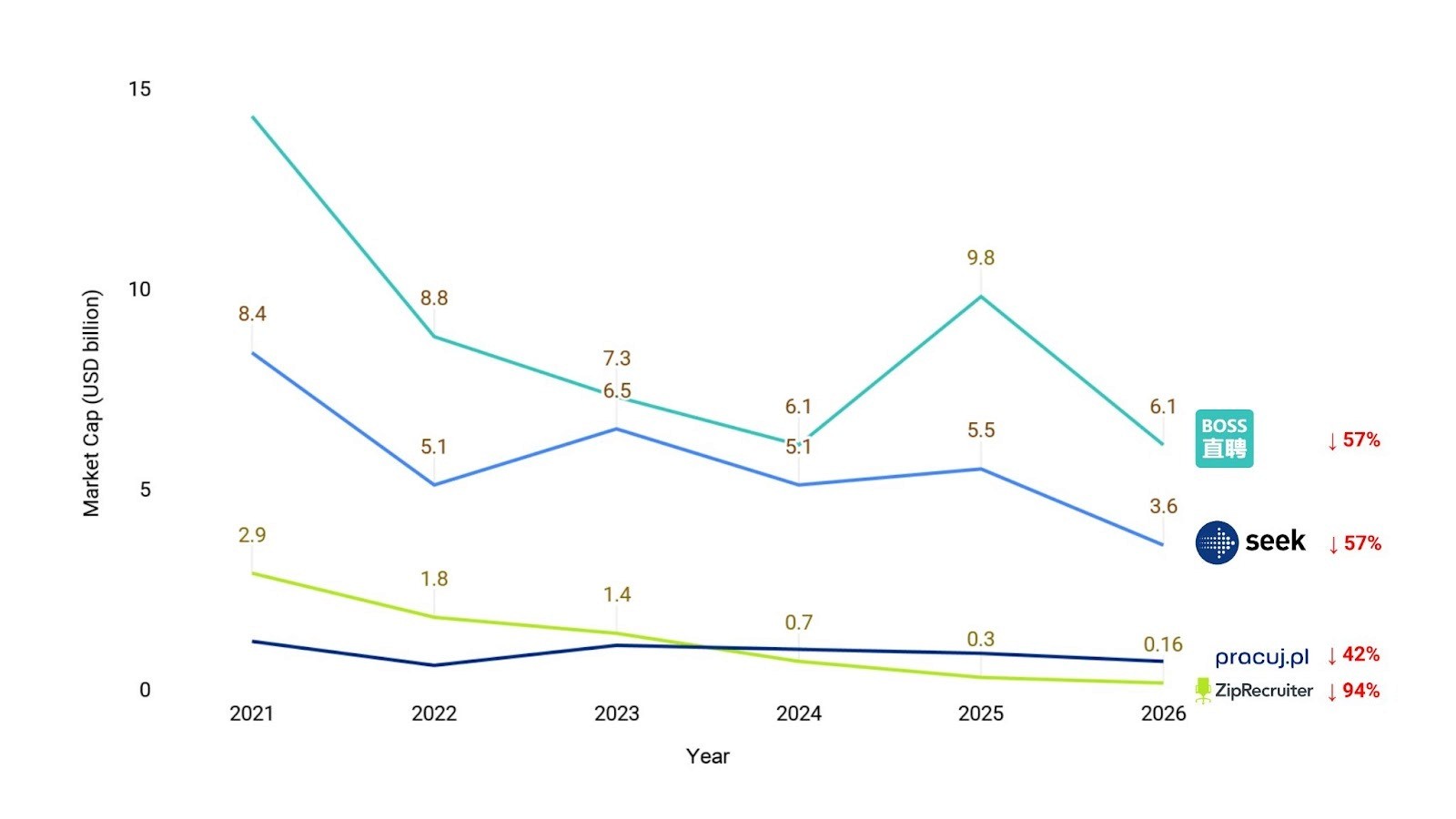

The chart above captures five years of value destruction across selected listed recruitment platforms: SEEK (Australia), Boss Zhipin (China), ZipRecruiter (US), and Pracuj (Poland). Collectively, these w companies have shed roughly $16 billion in market capitalisation since their 2021 peaks, despite a broadly resilient labour market and recovering equity markets.

ZipRecruiter, which listed at a $2.2 billion valuation in 2021, was trading below $250 million by March 2026, a 90% decline. Its revenue fell from $905M in 2022 to $449M in 2025, a 50% decline, during a period of full employment. When it announced a ChatGPT integration in March 2026, the stock fell further; investors no longer believe AI features can restore what has structurally eroded.

SEEK has seen its market capitalisation fall 57% between 2021 and 2026, from $8.4 billion to $3.6 billion. Revenue peaked at approximately $810 million in FY2023 and fell to $720 million in FY2025, an 11% decline, as paid job ads dropped 20% year on year in Australia and New Zealand. Despite capturing record applications per job ad, employers are posting less and using the channel less.

Recruit Holdings, owner of Indeed and Glassdoor, has invested aggressively in AI. In FY2023 the company disclosed US paid job advertisements on Indeed had declined approximately 50% year-over-year. Even after stabilising in FY2025, HR Technology revenue remains roughly 10% below its FY2023 peak ($7.4B in FY2025). In July 2025, Recruit’s HR Tech Division laid off approximately 1,300 employees.

What is eroding is the core model: post a job, receive applications, charge for access. That model was always dependent on candidates actively visiting job boards, which increasingly, they do not. The absence of better alternatives meant the model survived.

In the private markets, most notably former job board giants CareerBuilder and Monster - having only merged in 2024 - filed for Chapter 11 bankruptcy nine months later, saddled with $392.5 million in debt. Their core job board assets were auctioned off for $28 million.

Fast Forward to 2026

For over a decade, recruitment platforms created value by aggregating traffic, building databases, and monetising access. That model is now under threat.

The incumbent model depends on candidates actively searching and applying. The spread of one click applications and agentic auto apply are moving the value creation layer to the quality of the match and agentic fit assessment.

Furthermore, job boards appeal most to proactive, usually unemployed, candidates. AI opens up the rest of the market, the ~70% of candidates who are passively open to opportunities but are not visiting job boards. With AI, talent can be identified, evaluated, and matched before a job is even posted.

A three-year-old recruitment AI startup, Mercor, which connects reinforcement learning specialists with LLM and other AI companies raised $350 million in October 2025 at a $10 billion valuation, a fivefold increase in eight months, and told investors it was on track to hit $500 million in ARR. It had no salespeople, and its founding team averaged 22 years old.

Will new players capture the value AI opens up, or can incumbents pivot fast enough to grab it?

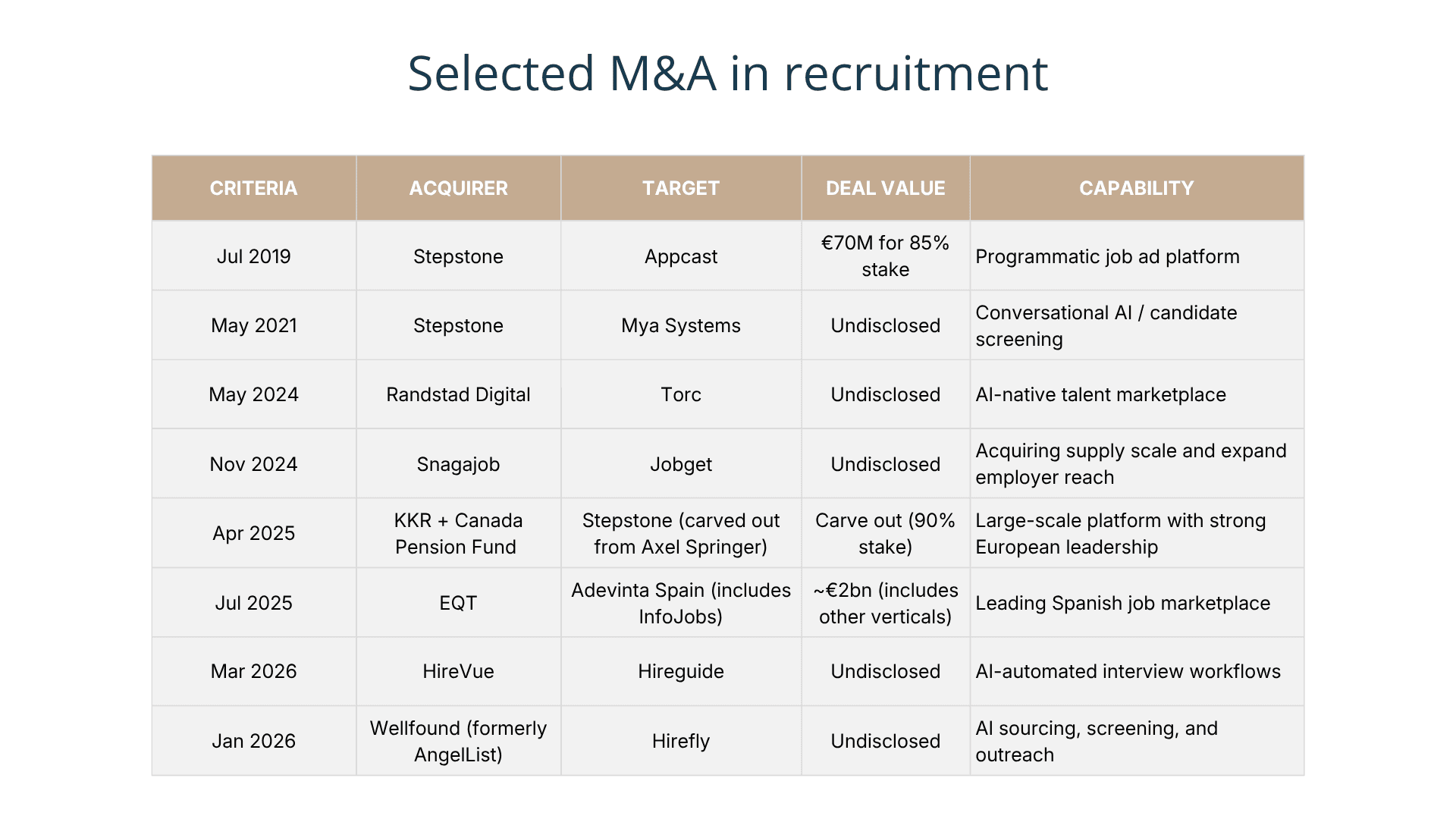

What is the M&A wave telling us?

Revenue model transformation: Stepstone acquired Appcast to shift beyond listing fees toward performance-based advertising. Employers were no longer willing to pay for access to candidates who might not apply.

Acquiring AI capabilities: Mya, Torc, Hireguide, Hirefly - job boards are acquiring AI capabilities that would have taken too long to build internally. These platforms bought AI workflows, AI candidate screening, AI matching, and AI intervie

wing capabilities. The incumbents were falling behind product parity with newer platforms and bought their way to feature completeness.

Distressed consolidation: In Nov 2024, JobGet acquired Snagajob,once the dominant US job board for hourly workers with 100M users, ~200K employer locations, and $387M raised, but down to just 3.6M MAUs by 2024. JobGet, founded in 2019, raised only $52M to reach a $440M valuation by 2022, built a mobile-first, instant-connect product, overtook Snagajob on engagement, and ultimately acquired it. A five-year-old startup, built with a fraction of the capital, absorbed the original market leader.

PE is still active, but the thesis has changed: KKR carved out Stepstone in 2025 with an explicit AI mandate and IPO endpoint. EQT acquired Adevinta's Spanish portfolio, which includes InfoJobs, the dominant job board in Spain. The playbook is shifting toward taking market-leading incumbents and rewiring them into AI-native businesses.

Where are the VC’s placing their Bets?

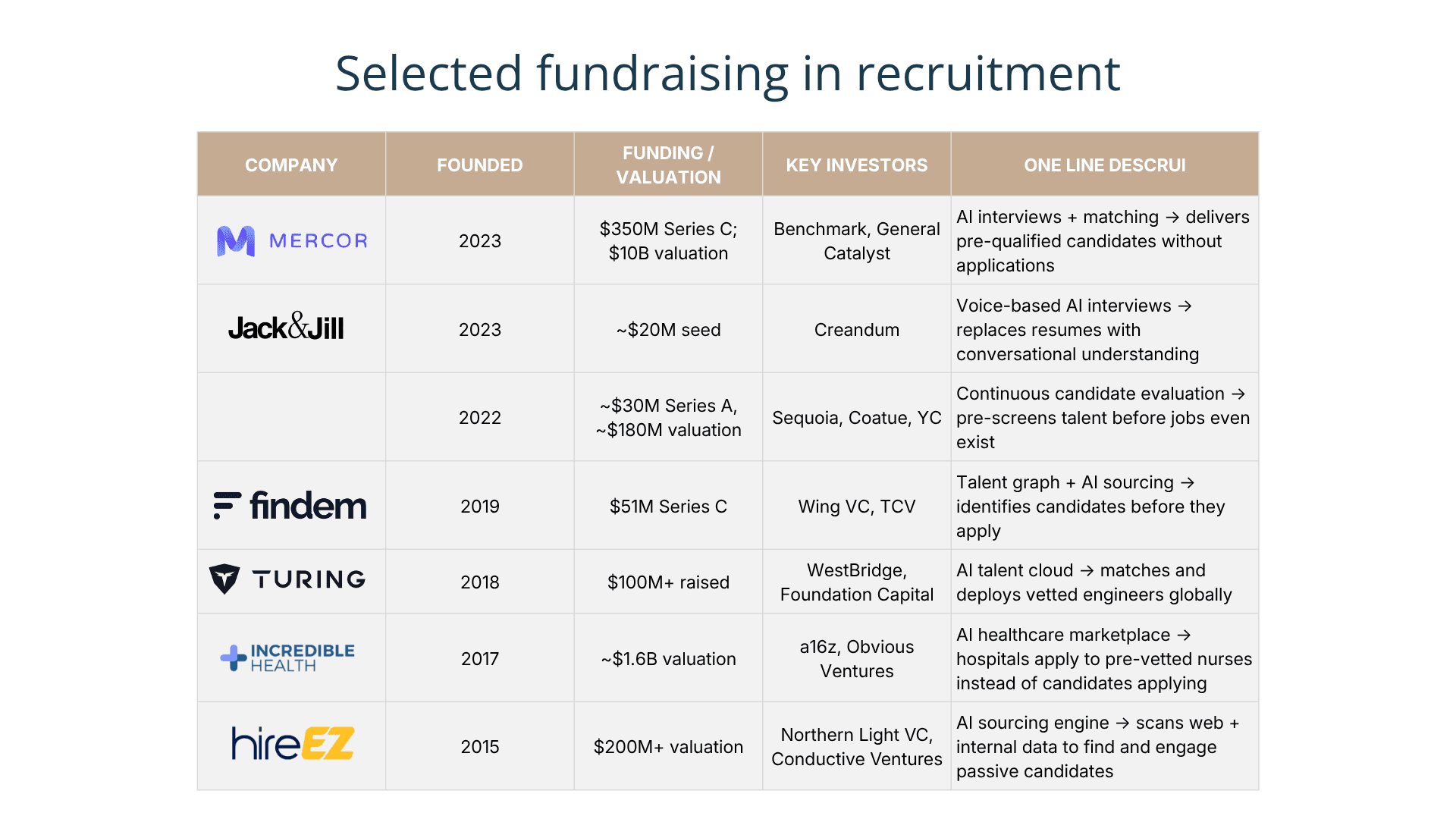

Capital is flowing into startups that are providing alternatives to job boards

Every company on this list: Mercor, Juicebox, Findem, hireEZ, Turing, Jack & Jill, Incredible Health, operates on the premise that candidates should not have to apply. The platform either sources them passively, interviews them proactively, or has them apply once and be continuously matched. The job board model: post a job, wait for applications, is absent from these investment theses.

AI is being used at the assessment and verification layer

Mercor does AI interviews. Jack & Jill does voice-based AI interviews replacing resumes. Incredible Health pre-vets nurses before hospitals see them. Juicebox continuously evaluates candidates before jobs exist. The investment thesis has moved beyond "find candidates faster" to "verifying capability".

Vertical specialisation

Incredible Health raised relatively modest equity but reached a $1.6 billion valuation because it owns a specific, hard-to-reach, credentialed community, pre-vetted nurses, in a market where hospitals have enormous pain around hiring speed and compliance

And What About the Other Giants?

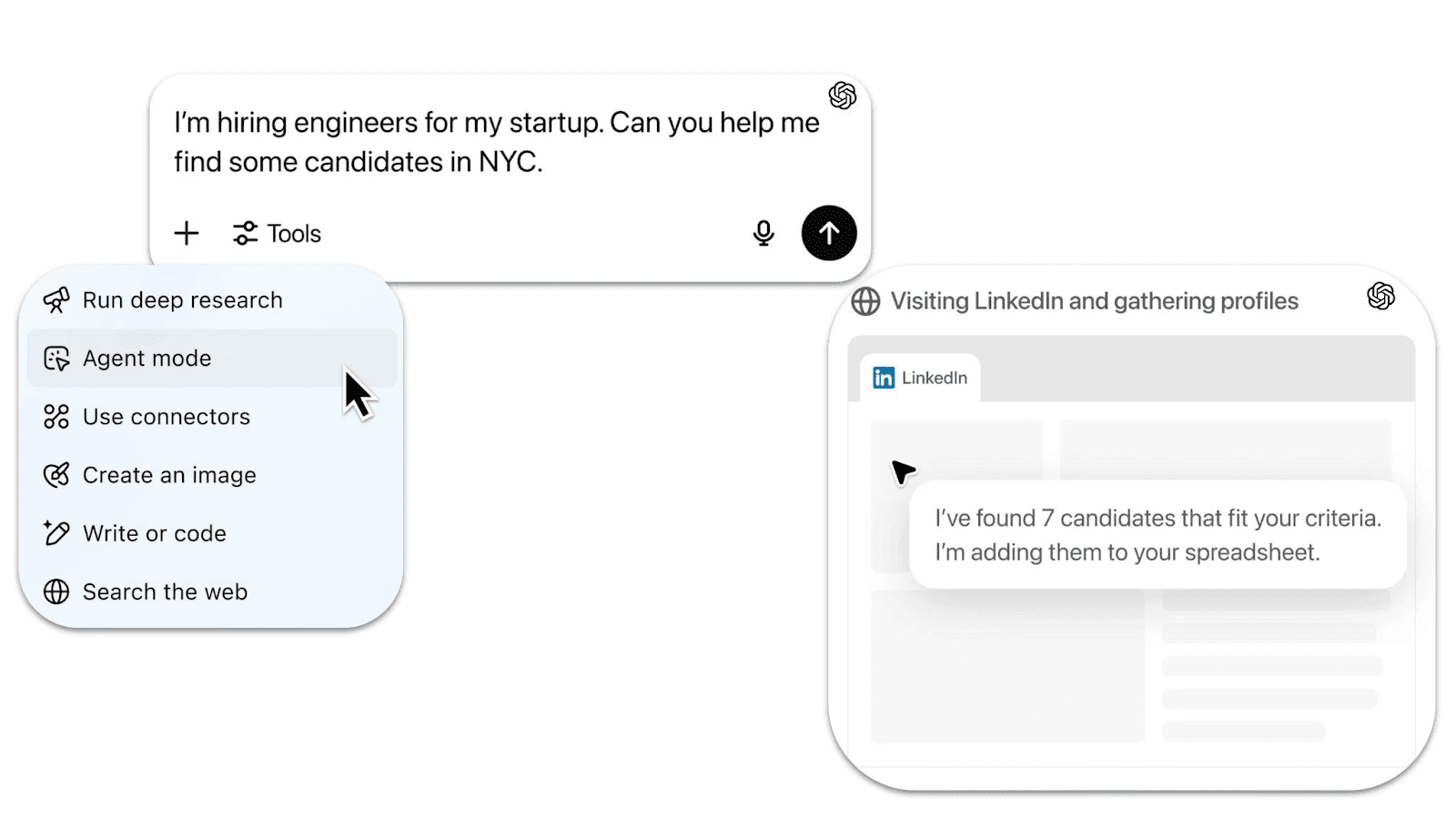

OpenAI is entering the market

OpenAI announced the OpenAI Jobs Platform in September 2025, targeting a mid-2026 launch. It promises to match candidates with employers based on demonstrated AI competencies, verified through certifications built directly into ChatGPT and its 900 million weekly users. Walmart is an early partner.

LinkedIn is getting stronger

LinkedIn is the one incumbent whose position strengthens as the sector disrupts. With over 1 billion members and two decades of career history, it owns the underlying data layer that AI models depend on: who people are, what they’ve done, and how they move across roles and companies. It sits upstream of the hiring process, where discovery happens before a job is posted. As AI tools shift recruiting toward outbound sourcing and continuous matching, they increasingly rely on LinkedIn’s data graph, either directly or indirectly.

At the same time, LinkedIn is layering AI across both sides of the marketplace. For recruiters, it is automating sourcing, outreach, and shortlisting within existing workflows. For candidates, it is moving toward AI-assisted discovery, profile optimisation, and application support.

What Comes Next?

Since 2020, no significant generalist job board acquisition has generated a demonstrable return; PE has flipped but not yet exited well; public companies have seen value evaporate. The activity looking most promising is in vertical specialists and AI-native platforms - structurally different businesses from the job board.

New players are capturing value faster than most incumbents can respond. Mercor, founded in 2023, is targeting $500M million ARR without a sales team, Findem grew 3x year-on-year and made two acquisitions in three months, and OpenAI is entering the market. None of them are building or buying job boards.

The M&A data, the VC investments, and the public market signals all point in the same direction: value is moving away from platforms that “own” listings and toward platforms that own the matching layer: verified identity, credentialed communities, hiring outcomes. The repricing of this sector is real, it is accelerating, and it is far from complete.

In our next piece, we will examine how incumbents are responding, which acquisitions and internal bets are gaining traction, and what a job board would actually need to look like to generate a credible exit in an AI-first world.