Jun 10, 2026

What Happened to Later-Stage European Marketplace Investments (2021-25)?

Last week, we looked at how early-stage marketplace founders navigated the post-2021 funding crunch. What happened to the growth and later-stage landscape?

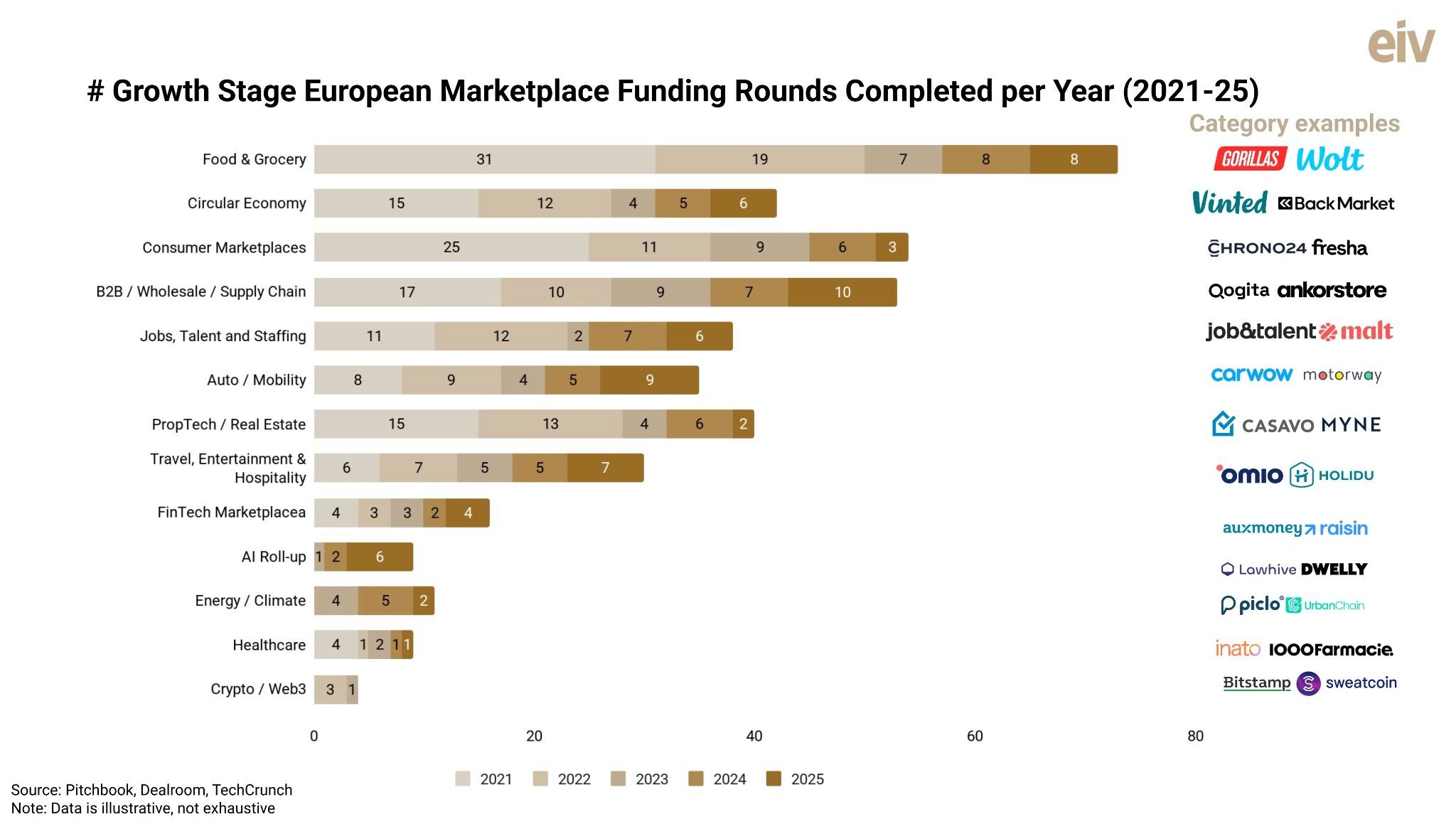

We examined 415 growth and late-stage deals (>$10M primary equity raised in a single round) across European platforms between 2021 and 2025, and mapped which marketplace sectors have seen declining capital raised since 2021, and which have seen growth.

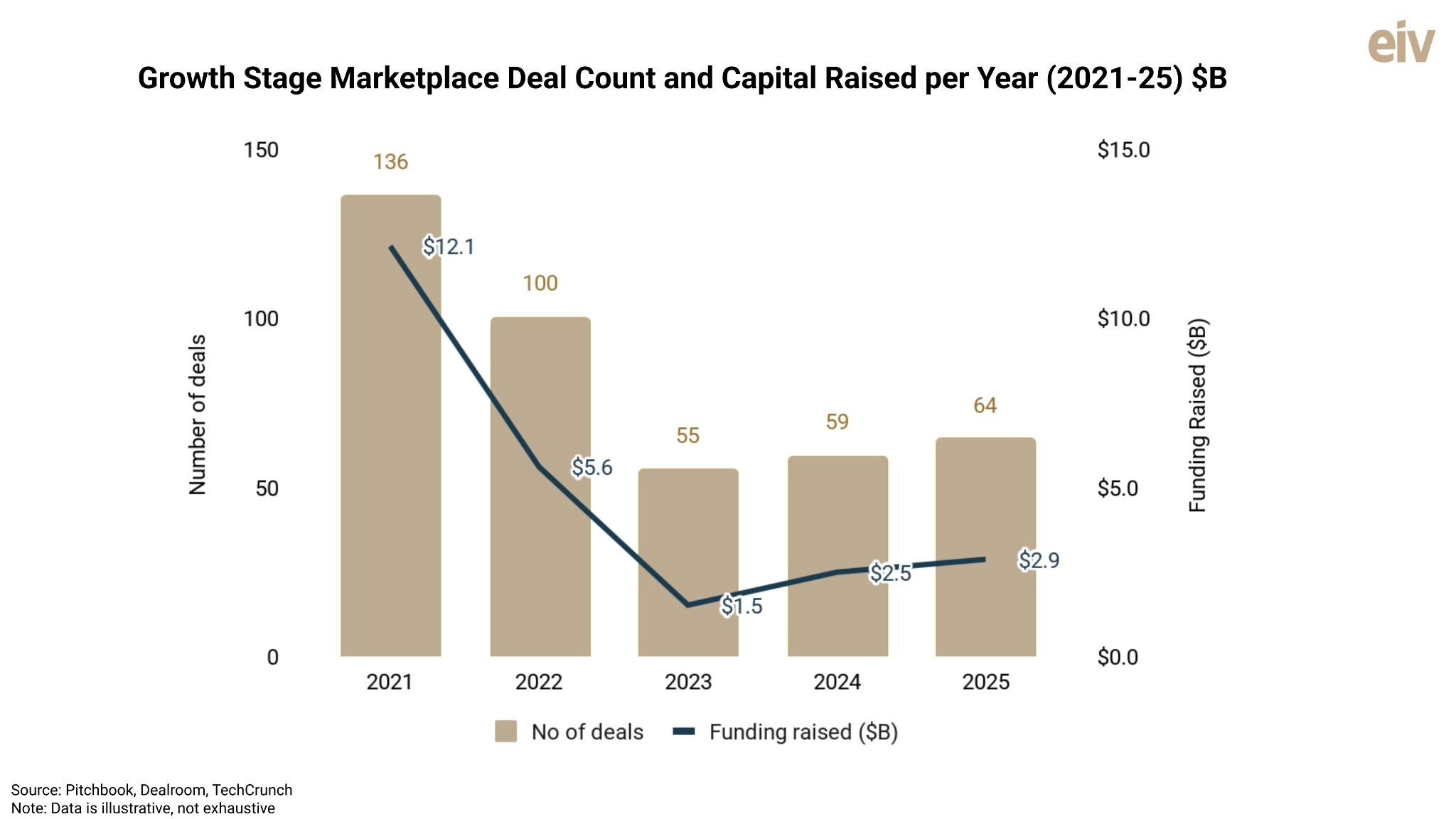

Growth and later-stage marketplace funding rounds fell from $12.1B in 2021 to just $1.5B in 2023, a drop of nearly 90%, before almost doubling to $2.9B in 2025. Deal volume followed, from 136 rounds in 2021 down to 55 in 2023, before rising to 64 in 2025.

We explore each vertical below.

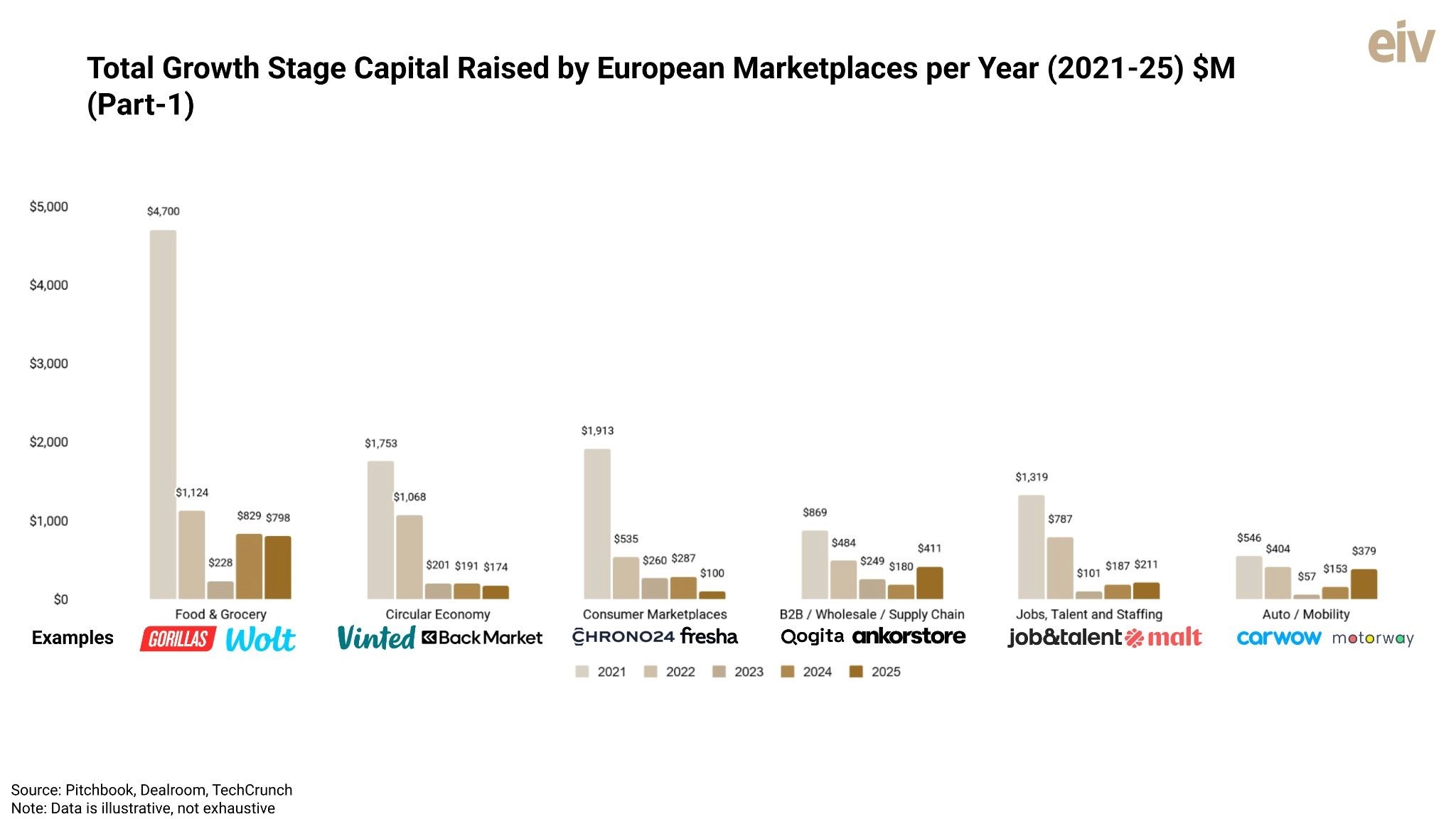

Food & Grocery

At $7.68B, food and grocery was the largest destination for marketplace growth capital 2021-25, but suffered a boom–bust–partial recovery pattern. Funding fell from a 2021 peak of 31 deals and $4.70B (representing more than a third of all late-stage marketplace capital deployed in 2021), to 8 deals and $798M in 2025.

The 2021 to 2022 peak was driven by quick commerce, the ten-minute, dark-store delivery startups that drew enormous rounds, including Gorillas ($950M and $295M in 2021), JOKR ($260M and $170M in 2021) and Zapp ($219M in 2022). By 2023, funding compressed to just $228M, and a wave of consolidation and market exits ensued: Gorillas was absorbed by Getir, platforms like Cajoo, Weezy, and Yababa shut down or were rolled up, and JOKR exited Europe.

By 2024-25, capital consolidated behind the survivors of instant delivery, evidenced by Flink's $150M stabilization round in 2024. Investors doubled down on highly optimized, app-only e-supermarkets and bulk delivery networks boasting superior unit economics thanks to larger baskets and less ambitious delivery time promises. This period saw funding rounds for Picnic ($498M in 2025 and $388M in 2024, app-only online supermarket), Rohlik Group ($170M in 2024, followed by $92M in 2025, online grocery delivery), organic membership grocery platform La Fourche ($37M in 2025), and sustainable milk-round delivery engine Modern Milkman ($27M in 2025).

Circular Economy

Circular economy was the second-largest growth category over the period, at $3.54B, falling from 15 deals and $1.75B in 2021 to 6 deals and $174M in 2025. The capital chased a small set of category leaders across two main verticals, fashion resale and refurbished electronics.

2021–2023, late-stage funding concentrated on large-scale consumer-to-consumer (C2C) marketplaces and electronics refurbishment aggregators. Investors poured hundreds of millions into asset-light matching platforms to capture a mainstream shift in retail habits. This era was defined by blockbuster financings for peer-to-peer fashion networks like Vestiaire Collective ($308M and $210M in 2021, followed by $142M in 2022) and Vinted ($306M in 2021). In electronics, this period saw scaling rounds for Back Market ($334M in 2021 and $542M in 2022, refurbished electronics marketplace), Swappie ($124M in 2022, refurbished iPhones), and Grover ($71M in 2021, tech rental subscription).

2025 saw no mega-rounds. There were mid-sized capital raises by Refurbed ($55M in 2025, refurbished electronics marketplace) and Grover ($55M in 2024). Meanwhile, category leaders like Back Market ($77M in 2024) and Vestiaire Collective ($23M in 2024) relied on smaller, lean tranches. The rest of the money rotated toward narrower, newer models, including Upway ($60M in 2025, refurbished e-bikes) and Rebike ($14M in 2024, used e-bike marketplace), Subbyx ($16M in 2025, device-subscription platform), and Mobile Club ($15M in 2025, smartphone rentals). This period also saw the rise of B2B circular marketplaces like Metcycle ($15M in 2025, B2B recycled-metals marketplace), Safi ($20M in 2023, B2B recyclable-commodities marketplace) and Resourcify ($14M in 2025, recycling marketplace).

Consumer Marketplaces

Consumer marketplaces saw amongst the steepest collapses in the dataset, from 25 deals and $1.9B in 2021, to just 3 deals and $100M in 2025. The capital went into vertical product marketplaces and consumer services.

Between 2021 and 2023, the largest sums went to education and product e-commerce. Online learning was the single largest destination, led by GoStudent (around $765M across four rounds, online tutoring marketplace), Ornikar ($118M in 2021, driving-school marketplace) and Keystone Education Group ($23M in 2021, student-to-university marketplace). Product e-commerce backed vertical category specialists, including ManoMano ($380M in 2021, DIY and home-improvement marketplace), Chrono24 ($118M in 2021, pre-owned watch marketplace) and Otrium ($122M in 2021, off-season fashion marketplace). Local-services booking marketplaces also got going, with Fresha ($153M in 2021, salon and spa booking marketplace), Planity ($35M in 2021, hair and beauty booking marketplace) and Playtomic ($59M in 2022, racket-sports booking marketplace).

GoStudent's last round was a smaller $95M in 2023.

From 2024 onwards, investors doubled down on the booking-services marketplaces first funded in 2021 and 2022 with Planity ($50M in 2024), Playtomic ($69M in 2025) and Fresha ( $80M Series C in May 2026) all raising again. A handful of new models raised growth capital for the first time, including Tiney ($14M in 2025, childcare marketplace), Tilt ($18M in 2024 and $26M in 2026, social and live-commerce app) and Fanvue ($22M in 2026, creator-subscription marketplace), while the largest recent consumer round went to Catawiki ($185M in 2024, established curated auction marketplace).

Jobs, Talent and Staffing

Jobs, talent and staffing raised $2.5B over the period, falling from 11 deals and $1.32B in 2021 to 6 deals and $211M in 2025.

The vertical was dominated by blue-collar staffing giant Job&Talent, who alone absorbed more than $875M across three blockbuster rounds in 2021, representing nearly two-thirds of that year's total capital within the vertical. This period also saw landmark deals including workplace apprenticeship platform Multiverse ($131M in 2021 and $220M in 2022), corporate-coaching marketplace CoachHub ($80M in 2021 and $200M in 2022) and generalist freelance and staffing networks like Malt ($97M in 2021 and $61M in 2022, freelance marketplace), Zenjob ($51M in 2022, temp staffing marketplace), and Orka ($40M in 2021, shift-staffing marketplace).

Job&Talent continued to raise with a $100M round in 2025. Elsewhere, sector momentum shifted into 1) AI-native hiring such as AI enterprise skills-intelligence platform TechWolf ($43M in 2024), automated hiring/interview platform Metaview ($37M in 2025), and AI recruitment platform Talentium ($11M in 2024), and 2) specialised staffing, AiScout ($23M in 2024, football scouting network), and healthcare, with Medwing ($47M in 2023, healthcare staffing marketplace) and TERN Group ($32M in 2025, global healthcare-workforce marketplace).

Auto and Mobility

Auto and mobility raised $1.54B over the period, with deal volume stable at 8 rounds in 2021 and 9 in 2025, while capital raised eased from $546M to $379M.

2021 saw successful rounds both for C2B and B2B transaction models such as Motorway ($142M in 2021, used-car C2B marketplace) and CarOnSale ($61M in 2021, B2B used-car auction). Growth also came from funding consumer-facing alternative ownership models including Virtuo ($97M in 2021, car-rental platform), consumer subscription models like Carvolution ($16M in 2021, $17M in 2022, all-inclusive car-subscription service), and ride sharing Comuto ($115M in 2021, the BlaBlaCar carpooling marketplace). By 2023, funding for large consumer plays had all but dried up, leaving a sparse landscape characterized by small, highly-localized growth rounds for niche plays like Karos ($19M in 2023, daily commute carpooling), Mundimoto ($12M in 2023, online motorbike marketplace), and Blinto ($11M in 2023, vehicle auction marketplace).

By 2025, the largest rounds went to LIZY ($87M in 2025, used-car leasing for SMEs), CarOnSale ($81M in 2025), the corporate chauffeur platform LimoLane ($80M in 2025) and Spotawheel ($30M equity in 2025, full-stack used-car marketplace) amongst others.

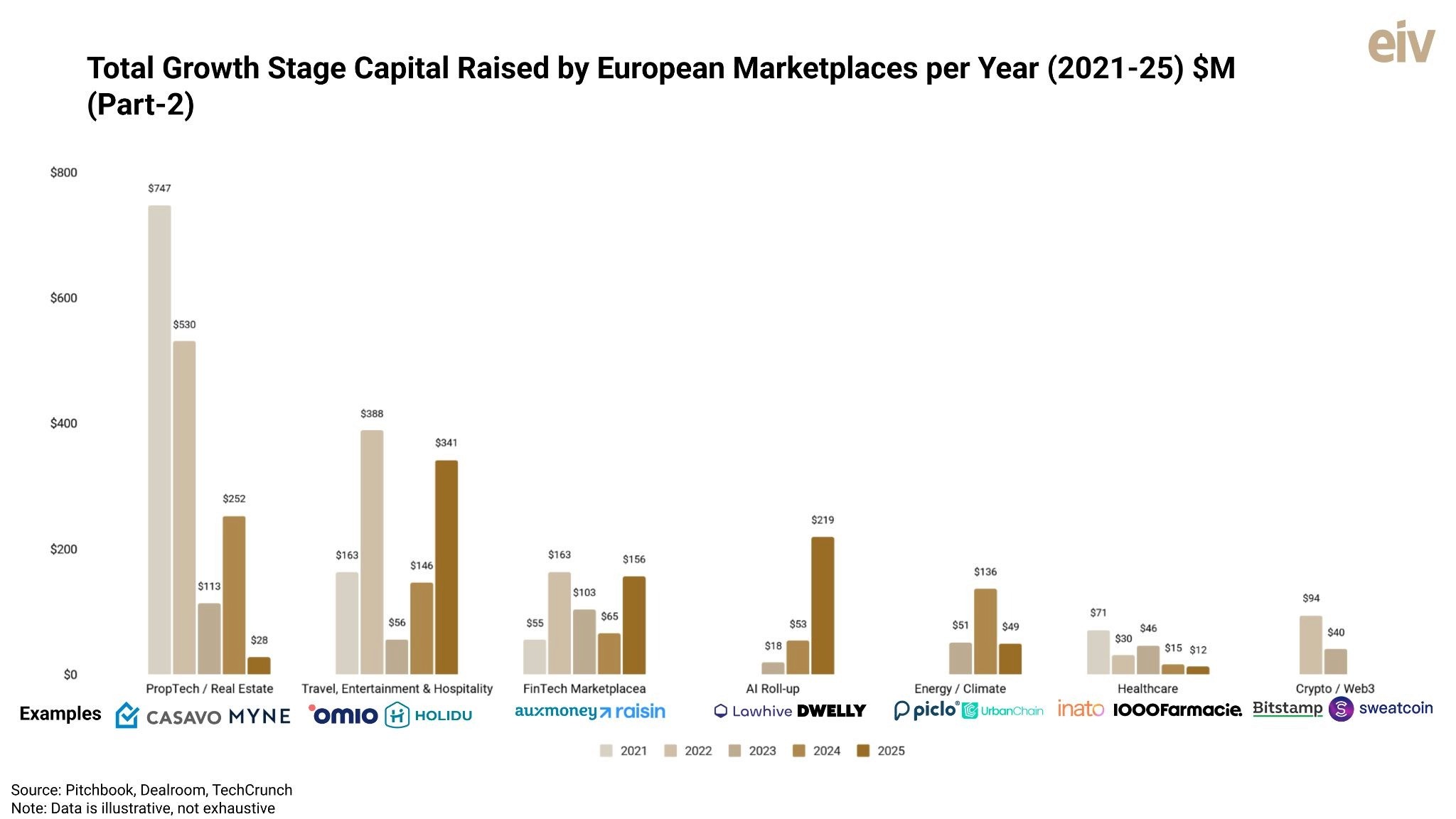

PropTech and Real Estate

PropTech and real estate fell from 15 deals and $747M in 2021 to 2 deals and $28M in 2025, one of the steepest collapses in our dataset.

The 2021–2022 peak was dominated by property iBuyers, co-living developers, and furnished apartment managers, including iBuyer Casavo ($59M in 2021 and $102M in 2022) and Clikalia ($79M), premium furnished rental provider Blueground ($180M), co-living manager Cohabs ($110M in 2022), alongside property-lending plays like Property Bridges ($118M, peer-to-peer property lending). The equity figures understate these models, since the iBuyers raised far more in debt to buy and refurbish homes.

As interest rates rose, the iBuyer model broke, Casavo largely abandoned iBuying in 2023 to become an asset-light brokerage. However, the co-living model sustained with continued investment in Cohabs ($142M in 2024), and into a new fractional and co-ownership thread in second homes, including MYNE ($43M in 2024, holiday-home co-ownership marketplace), Fractal Homes ($30M in 2023, fractional luxury-home marketplace) and Vivla ($28M in 2023, fractional second-home marketplace). The rest was small and capital-light, led by Zefir ($18M in 2025, home-selling marketplace).

B2B, Wholesale & Supply Chain

The B2B wholesale and supply chain vertical fell from 17 deals and $869M in 2021 to 10 deals and $411M in 2025.

The early rounds were large, including Gelato ($240M in 2021, B2B print-on-demand platform), Ankorstore ($283M in 2022, B2B horizontal wholesale marketplace), Mercell Holding ($97M in 2021, B2B e-procurement marketplace), and Qogita ($87M in 2023, B2B wholesale marketplace for consumer goods).

After 2022, the mega-rounds stopped, but mid-sized financing continued steadily as procurement and wholesale digitisation went on, with recent rounds for Blk Global ($63M in 2025, B2B commodities and raw-materials marketplace), SOS Accessoire ($53M in 2024, B2B spare-parts marketplace), Relay Technologies ($34M in 2025, B2B last-mile delivery marketplace), and, into 2026, Andercore ($47M in 2026, AI-powered B2B marketplace for industrial and building materials), Easy2Parts ($13M in 2025, AI general spare parts marketplace) and Nivoda ($50M in 2024, B2B diamond marketplace).

The fastest-growing new category in B2B is the emergence of AI-native service platforms, which deliver AI-native services rather than matching buyers and sellers. Legal services led, with Legora ($150M and $80M in 2025, and a further $600M in 2026, AI legal platform) and Wordsmith ($70M in 2026, AI legal-assistant platform) raising the largest B2B rounds of the whole period.

Travel, Entertainment & Hospitality

Travel, entertainment and hospitality is a good recovery story, more than doubling from $163M in 2021 to $341M in 2025. With the pandemic finally over, capital migrated from holiday rentals to campervans, curated tours, serviced stays and live events.

The early phase funded holiday-rental and multimodal booking, including Holidu ($45M in 2021, $102M in 2022, holiday-rental marketplace), and Omio ($178M in 2022, multimodal travel-booking marketplace).

From 2024 the money spread to marketplaces like Indie Campers ($71M in 2025) and Roadsurfer ($31M in 2025), Exoticca ($65M in 2024, curated-package travel marketplace), Seat Unique ($21M in 2024, sports and live-event ticketing marketplace). Already in 2026, we have seen rounds announced for WeRoad ($53M, group-travel marketplace) and Naboo ($64M, corporate-events platform).

Other Verticals: FinTech, AI Roll-ups, Healthcare and More

FinTech marketplaces raised $542M across 16 rounds over the period. Lending and deposit marketplaces include InSoil ($113M in 2025, crowdlending marketplace connecting investors with farmers), Raisin ($64M in 2023, marketplace connecting savers with banks offering deposit accounts), Auxmoney ($53M in 2024, marketplace connecting consumer borrowers with investors) and Capitalise ($18M in 2021, marketplace connecting SMEs with business-finance lenders).

Among the rest, healthcare raised $174M across 9 rounds; in particular online pharmacy and clinical-trial matching, including 1000Farmacie ($25M in 2023, Italian online pharmacy marketplace) and Inato ($21M in 2023, clinical-trial-site marketplace).

Energy and climate remained small at $236M 2021-25, peaking in 2024 with UrbanChain ($65M, peer-to-peer energy marketplace). Crypto and web3 produced only four qualifying growth rounds in the entire period, all in 2022 and 2023, including Bitstamp ($40M in 2023, crypto exchange) and SingularityNET ($25M in 2022), and none since.

AI roll-ups are the newest model at the growth stage, and one to watch. The category raised $290M across 9 rounds between 2023 and 2025, including Buena ($57M in 2025, AI property management), Jutro Medical ($42M in 2025, AI primary-care clinics), Dwelly ($59M in 2025, AI lettings and property management), Arbio ($36M in 2025, AI short-stay management) and Numeris ($33M in 2025, accounting-firm roll-up). These are more platforms than marketplaces. The operators buy fragmented local service businesses in property, legal, accounting and primary care, then migrate them onto a common AI-native operating layer. The momentum has carried into 2026, with Dwelly ($43M in 2026) and Lawhive ($59M in 2026, AI legal-services platform) already raising larger rounds.

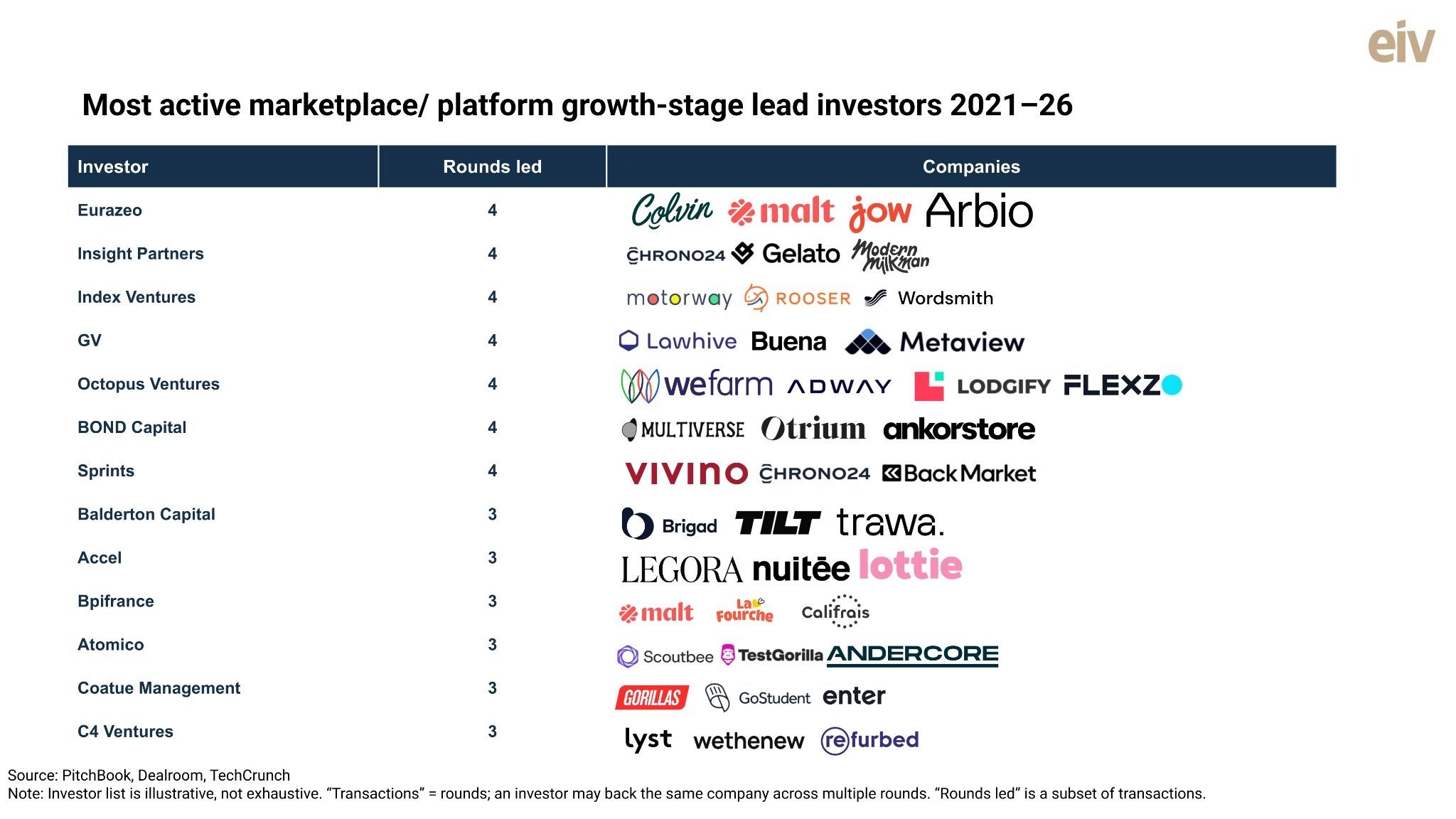

Who are the most active growth-stage marketplace investors?

A small group of funds show up as serial later stage marketplace investors. The most active by deal count is FJ Labs, the New York marketplace specialist, which appears in 38 rounds in our selected dataset. Other frequent growth stage marketplace investors include Accel, Atomico, Balderton, Bonsai Partners, Bpifrance and Speedinvest.

The most frequent lead investors are Sprints, Eurazeo, Insight Partners, Index Ventures, GV, Octopus Ventures and BOND Capital, each leading three or more rounds in our dataset, followed by Accel, Atomico, Bpifrance and General Catalyst. FJLabs does not lead.

The largest rounds also pull in global crossover and private-equity capital including Coatue, Tiger Global, General Atlantic, DST Global, Baillie Gifford, TPG and EQT.

Some Takeaways for Founders

2025 was definitely a better year to launch a marketplace growth round than 2023/4. Raising a growth round today demands a sharper category focus, and more compelling unit economics earlier on than it did in 2021. We are seeing a far higher number of managed and transactional marketplaces. These are the types of marketplaces (in comparison to say pure lead gen models like classifieds and price comparison), where it is possible to demonstrate to investors that AI will turn the marketplace flywheel faster, via better matching of supply and demand, and by taking out friction points and costs.

EIV advises marketplace and platform founders raising growth capital. If you are a marketplace founder approaching Series B, or later, we would love to hear from you.