Jul 15, 2026

Why over the past year have public markets been rewarding some marketplaces while punishing others?

Marketplaces have delivered stellar returns for decades. This week we uncover what has happened to those valuations over the past 12 months, and where the repricing seems justified — and where less so.

Since mid-2025 public markets have become less enthusiastic about businesses whose economics depend on attracting traffic and selling leads, particularly classifieds and portals. At the same time, they have become increasingly bullish on marketplaces that own unique supply or facilitate the transaction itself.

That distinction has driven some of the largest valuation moves in the sector. Property portals and lead generation businesses have seen multiples compress despite, in many cases, continuing to deliver solid operating results. Transactional marketplaces in categories such as wholesale automotive, resale and commerce have generally been rewarded.

Below we take a look at five marketplace sectors — Automotive, PropTech, Consumer, Circular Economy and Food & Grocery, to understand how investors are repricing core marketplace verticals in 2026.

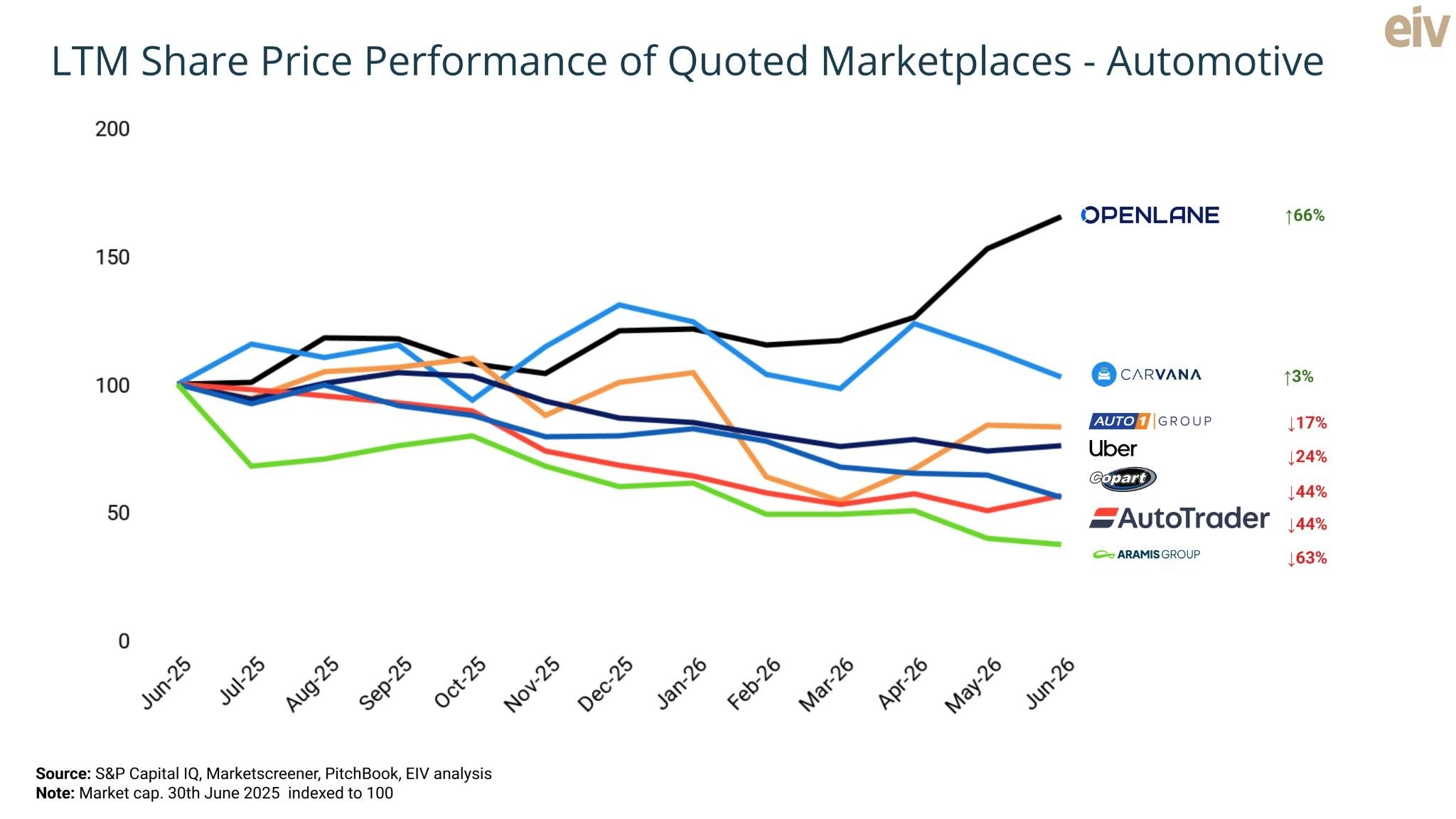

Automotive

Having produced many of the last decade’s post IPO winners up until June 2025, quoted automotive marketplaces have shown highly varied performance over the last 12 months.

OPENLANE is the standout winner, up 66%, as dealer-to-dealer activity rebounded after two unusually weak years. B2B sales of used cars is a complex business and one where AI is more likely to enhance the profitability of well-entrenched players than challenge them with wholly new transaction models.

Carvana, the top quoted marketplace performer of the decade to June 2025, finished the 12 month period up 3%, pausing for breath after a >100x recovery since December 2022.

AUTO1 fell 17% despite another strong operating year. The company delivered record volumes and profits, but investors questioned whether the exceptional per-unit economics achieved in late 2025 were sustainable. AUTO1 seems well-placed to build a “Carvana-like” business across the EU, but currently has earned only ~12% of Carvana’s valuation.

Uber has lost 24% of its value despite bookings growing 20%. The market is pricing a potentially existential threat on market share from robotaxis, such as from Waymo. If Uber can become the aggregator of robotaxis they seem well placed to benefit as the technology rolls out geographically. Uber’s pursuit of Delivery Hero is possibly also affecting investor sentiment.

AutoTrader fell 44% despite reporting revenue growth and stable margins. With a forward EBITDA multiple of around 10, AutoTrader has been heavily impacted by the AI-fuelled derating of the world’s best positioned and best monetizing classifieds platforms. We are yet to see any company on the horizon likely to move meaningful demand away from AutoTrader. Once the company starts to show enhanced user experiences and new revenue streams enabled by its AI product focus, investors might start to reconsider.

Aramis, Europe's leading online used-car retailer, fell 63% as high financing costs, weak consumer demand and manufacturer incentives on new vehicles weighed on Europe's used-car market. The company exited unprofitable UK activities and underwent operational restructuring in Austria, contributing to volume declines of 18% and 35% respectively.

PropTech

Lead gen models have been punished by investors during the past 12M. Some company specific catalysts have played a role - such as unprecedented legal scrutiny and pushback from real estate agents against Rightmove. CoStar’s spate of residential acquisitions and subsequent aggressive marketing spend has also unsettled investors. Sector-wide, the market appears to have concluded that even the best positioned property portals will suffer from AI-fuelled disruption. We think they have been too hasty: there is no evidence yet that LLM’s are syphoning off agency spend to the detriment of portals.

CoStar fell 65% in the last 12 months, and 27% in February alone, despite growing revenue by 20%. The market questioned whether Costar's core commercial real estate data business will be commoditized by AI. Investors also worry whether CoStar's multibillion-dollar investment in Homes.com and Domain will ever generate attractive returns. While we hold some sympathy for the former view, CoStar's CRE data is largely proprietary and hard to copy, and is likely to continue to generate strong cashflows.

Zillow has fallen 54% in the past year, despite growing revenues 16% in 2025 to $2.6bn and beating EPS expectations in its Q1 2026 results. Unlike Rightmove or ImmoScout, Zillow has grown up without exclusive for sale supply. Investors appear to be fretting about a combination of LLM-based disintermediation plus market consolidation of TEBs like Redfin leading to exclusive listings bypassing Zillow. On the other hand, few portals have invested more in re-imagining themselves for an AI-first world and LLMs continue to account for under 2% of visits.

Rightmove fell 48% over the LTM. Unprecedented legal action from real estate agents, combined with growing concerns that AI could bypass portals and squeeze lead-generation revenues, appear to be driving the decline.

Scout24 fell 41% despite revenues up 14%, net income up 37% and the company returning €455M to shareholders. The stock became another casualty of the sector-wide rerating as investors questioned the long-term value of portal traffic in an AI-first world. ImmoScout is arguably the most advanced national leader in embracing AI throughout organization and offer, and is perhaps the most likely to wrongfoot the bears.

Hemnet fell 75% despite a 50% EBITDA margin. The market reacted to a) concerns the seller-pay-per-listing model is overly exposed to AI disintermediation, and b) in February 2026, Sweden’s largest brokerage began routing listings to Booli, whose free-listing model offered an escape route for agents and buyers frustrated by Hemnet’s price increases. Looking back things don’t look so bad: average revenue per listing rose almost sixfold in 6 years, from SEK 1,414 to SEK 8,175, including a further 28% increase in 2025 alone.

Opendoor, is the outlier, up roughly 11x. A viral hedge-fund thesis made it 2025's meme stock, and the September appointment of Shopify's Kaz Nejatian as CEO, along with founder Keith Rabois returning as chairman, added 78% in a single day. We remain skeptical whether an inspired CEO, a high profile chairman and AI can transform what everywhere else has shown to be an economically unviable business model.

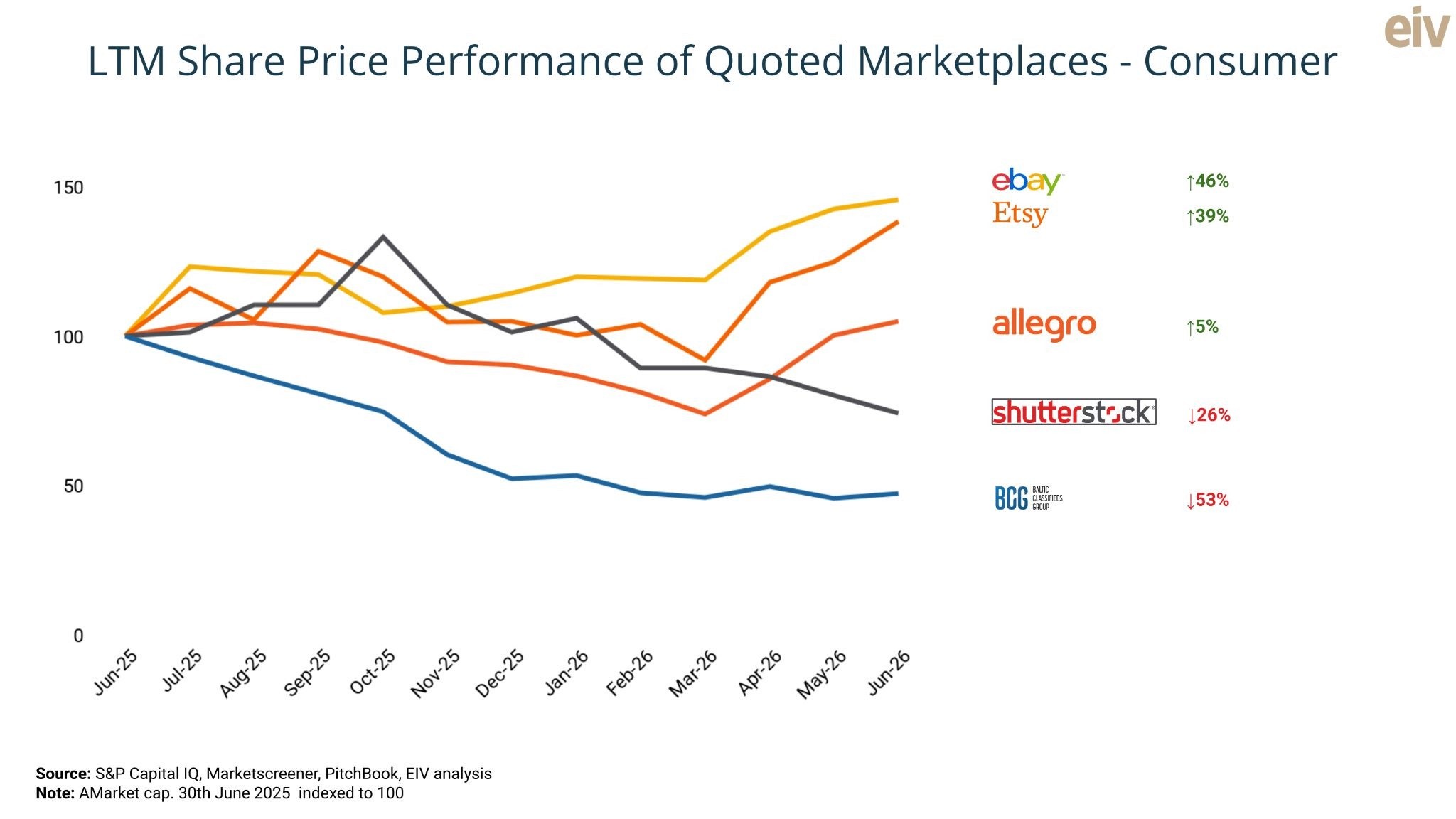

Consumer

eBay has risen 46% to $50bn in the LTM. Its GMV growth was driven by a pre-loved and collectibles boom, with category GMV accelerating from +1% to +18% by Q1 2026 following the launch of AI card scanner (in Q4 ‘25), which allows sellers to identify, value and list cards from a simple photo, helping unlock dormant inventory in one of the platform’s fastest-growing categories. At the same time, AI-generated listings from a single photo (launched in Q4 2025) became the default for new US sellers. The market is increasingly valuing platforms that own unique supply; given that pre-owned inventory is one thing an AI shopping agent must route to rather than around.

Etsy rose 39%, including a 16% single-day jump on 29 September when OpenAI launched Instant Checkout with Etsy sellers. Handmade and vintage inventory exists nowhere else; for Etsy, the AI layer arrives as a new demand channel rather than a threat.

Allegro added 5% despite losing its position as Poland’s most-visited shopping platform to Temu. Rather than competing with Temu on price, the company invested in its delivery and logistics, growing Allegro Delivery network (36,000+ lockers) which now handles 45% of parcels, and kept scaling Allegro Pay, which financed ~16% of Polish GMV.

Shutterstock lost 26% by June 2026, when the UK competition authority's divestiture demands killed the $3.7B Getty merger. The merger was to license the combined archives to AI labs. Standalone, the question is what a generic stock-content library is worth when models produce often very similar content for free.

Baltic Classifieds halved (−53%) during the period, taking its market cap to the level of its IPO 5 years ago. Revenues have doubled since. The market aggressively sold off the stock after management warned that investments into data and AI product upgrades would inevitably compress margins, compounded by auto tax changes in Estonia that stalled consumer-to-consumer vehicle listings - in our view temporarily. Estonians will still need a platform to sell their used cars… Given BCG’s 77% EBITDA margins, that leaves considerable scope to invest in product and tech and still deliver margins well over 60%.

Circular Economy

Having spent the first half of the decade somewhat out of fashion, quoted circular fashion marketplaces have performed well. Perhaps the ca. $10B valuation recently put on Vinted has helped to raise investor interest levels?

The RealReal, the pre-owned luxury fashion consignment marketplace is up 176% to $1.5B as the company successfully restructured its debt, optimized its consignment fee structures, and delivered positive, adjusted EBITDA. It is starting to prove that luxury fashion consignment models can be structurally profitable.

1stDibs, a high-end vintage and antique goods marketplace, rose 50% on its first-ever positive EBITDA quarter and steady buybacks. The company saw a strong rebound as higher average order values (AOVs) and cost-discipline improved its bottom line.

ThredUp, the mass market consignment fashion marketplace slipped 5% in the last 12M, after a 13x rally off its October 2024 low., while the business itself kept improving: revenue grew 15%, active buyers reached a record 1.4m, and adjusted EBITDA more than doubled to roughly $35m. Tariffs and the closure of the de minimis exemption also shifted some budget shoppers away from Temu and toward resale. We expect investors to continue to find favour with the ThredUp model

Nevertheless, all three names remain below their IPO marks; the shift is from pricing the model's unproven nature to pricing its viability as it scales.

Food & Grocery

Delivery Hero grew 57% in the last 12 months. Improving EBITDA margins, the successful IPO of Middle Eastern subsidiary Talabat, and Uber's stake increasing to 19.5%, fuelling takeover speculation led to the stock rally.

DoorDash fell 23% in the same period. In November, the management announced it would spend 'several hundred million dollars more' on a unified tech stack, autonomous delivery and merchant software, and the stock fell 17% the next day. Additionally, the platform faced regulatory headwinds, most notably in cities like Seattle, where mandated driver wage hikes forced apps to add regulatory fees, resulting in lower customer tips and suppressed order frequency.

Instacart drifted down 5%. Advertising revenues and software products continued growing, but investors increasingly questioned the position of a third-party intermediary caught between Amazon, Walmart and retailers building their own digital channels.

So what does this all mean?

Stock market movements reveal the concerns and opportunities investors read into the long established marketplace business model. In the last 12 months, unique supply (eBay, Etsy, The RealReal) was rewarded, while discovery layers, especially classifieds, were repriced from concerns of disintermediation and AI-fuelled challengers. Businesses embedded deeper into transaction workflows, such as OPENLANE, RB Global and Carvana, have been less impacted.

We think the sellers of classifieds have gone too far. Many of the most heavily punished businesses continue to deliver double-digit revenue growth, expanding margins and returning capital to shareholders throughout the sell-off. Property portals in particular are being valued on the assumption that consumers will delegate one of the largest and most emotional purchases of their lives to an algorithm. That remains a bold assumption.

At EIV we have been involved in the creation of some of Europe's most successful marketplaces. Unlike many SaaS businesses, marketplaces which aggregate unique supply and simplify and facilitate complex transactions, are likely to end up net beneficiaries as AI drives better matches, lower costs, and more compelling services.

If you own or operate a public marketplace and would like to continue the discussion, we would love to hear from you.

Disclaimer: EIV does not own or trade in public stocks; all opinions cited above are only to stimulate intellectual curiosity and debate, and in no event to be seen as recommendations to buy or sell.