May 28, 2026

Our Take on European Electronics Recommerce

Where a Managed Marketplace wins over Peer-to-Peer

A consumer buying a used phone in Europe today encounters two fundamentally different models. On horizontal classifieds like Leboncoin, as well as on semi-verticalized Vinted, transaction remains peer-to-peer: the platform facilitates discovery, payments and dispute resolution, but responsibility for the condition and quality of the device ultimately sits with the seller. That model works well in categories where products are inexpensive, easy to assess and relatively low-risk to buy secondhand.

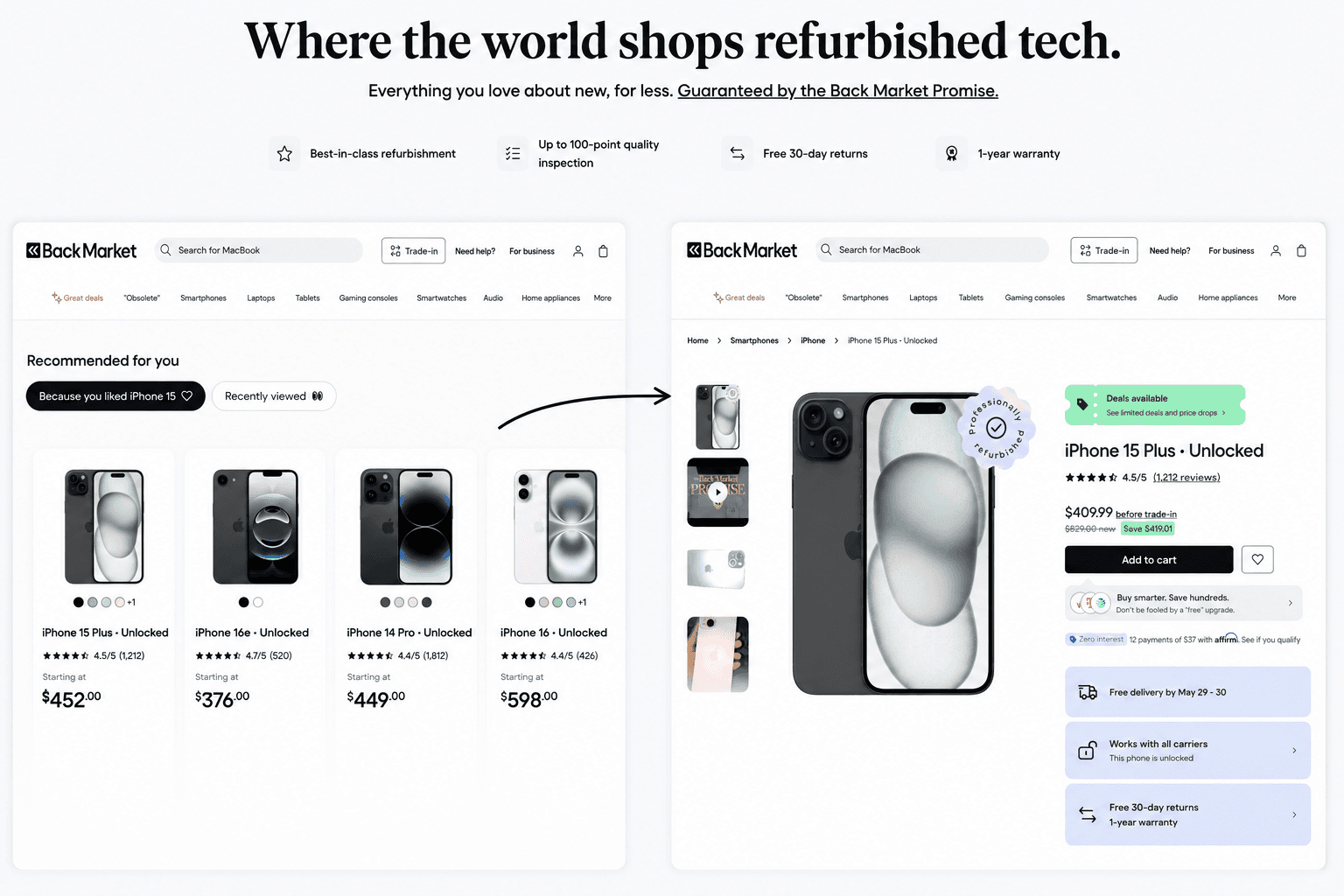

A €400 used smartphone is technically complex, and difficult to inspect remotely. This raises the trust threshold materially. As a result, specialists such as Back Market and Refurbed have built a vertical-specific, managed marketplace layer around the transaction: phone-specific taxonomy (screen size, memory etc.), condition grading systems, battery-health guarantees. This is then strengthened further by certified refurbisher onboarding, marketplace-issued warranties, returns handling, and a single point of accountability if something goes wrong.

The economics of reselling smartphones and laptops can fund a managed marketplace layer that most secondhand categories cannot / need not. The average order value is higher (typically €200 to €600), the product is technically complex (battery health, IMEI history, screen integrity, software support remaining), the purchase frequency is low (every two to three years), and the trust threshold to spend €400 on a phone the consumer cannot physically inspect is correspondingly higher than for a €15 dress or a €40 chair.

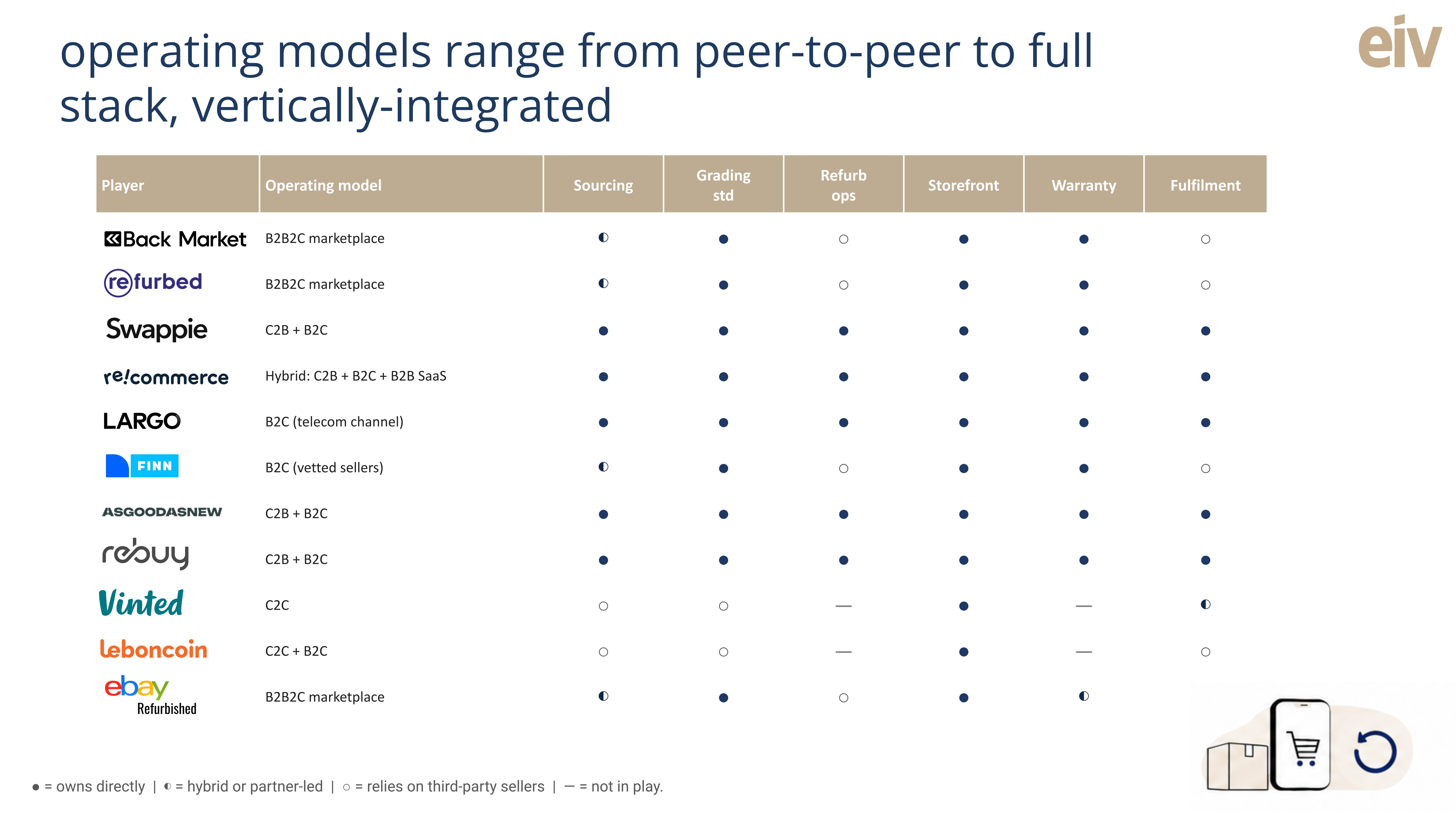

European electronics recommerce operates with four distinct business models that require very different amounts of capital to scale. We examine these next: European electronics recommerce operates with four distinct business models that require very different amounts of capital to scale. We examine these next:

Asset-light Marketplaces

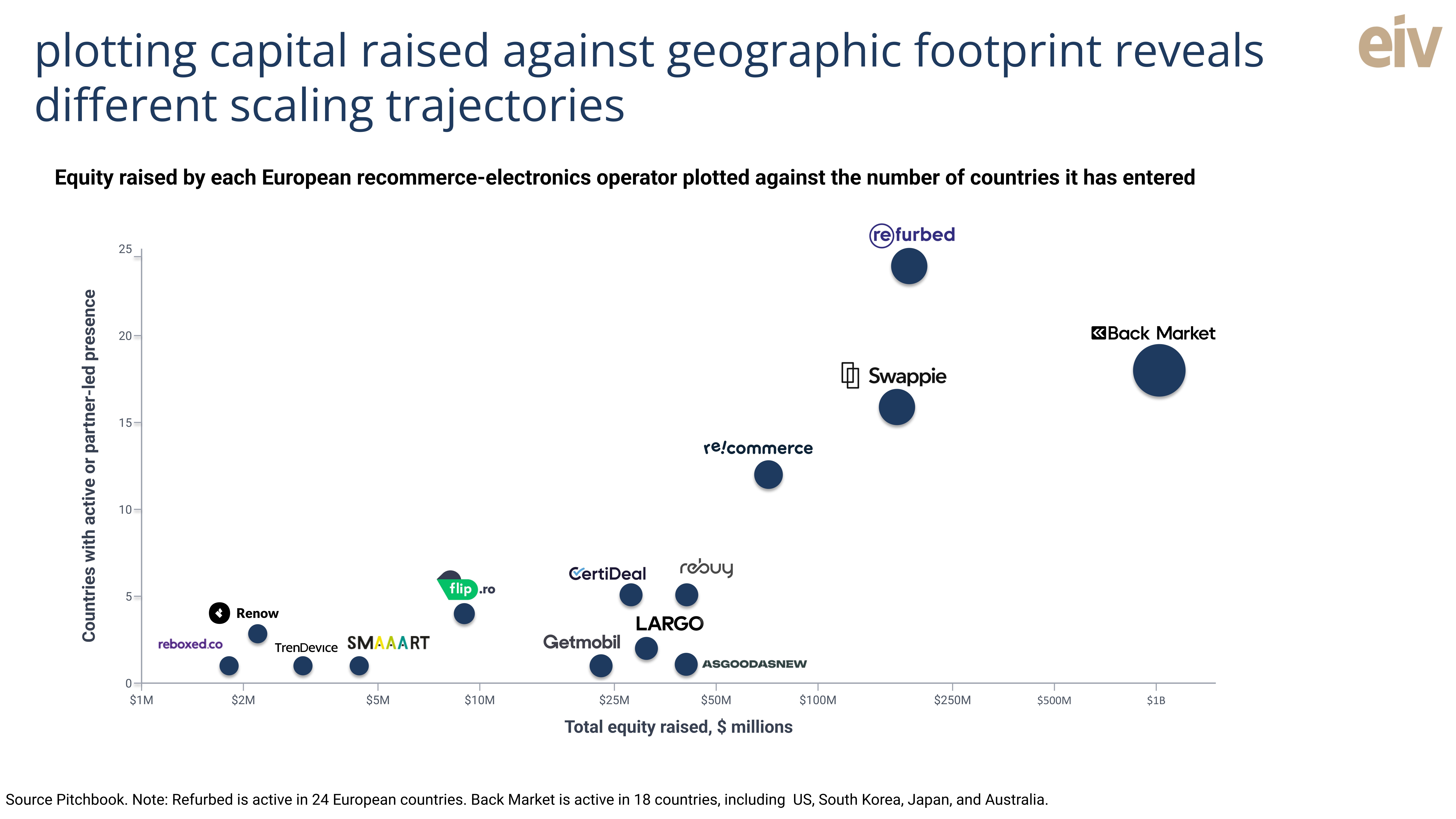

Back Market and Refurbed are pure B2B2C electronics marketplaces. Neither holds inventory directly. Approximately 2,700 vetted professional refurbishers (Back Market) and a comparable supply network (Refurbed) list devices on the platform, with the platform setting the quality charter, the grading scale, the warranty terms, the returns policy and the trust infrastructure including mystery shopping, fraud detection and payment processing. Refurbed (founded in 2018) reached EBITDA profitability in March 2025, having raised approximately $186 million; a further €50 million Series D closed in October 2025 tagged specifically to the UK launch, broader product categories and AI-driven platform investment. Back Market (founded in 2014) reached profitability in FY2025 after having raised approximately $1 billion across six rounds from 2014 to 2022. The capital requirement comes from building two-sided liquidity for a low-frequency trust-led purchase, absorbing the warranty and fraud costs, and replicating that stack across multiple European countries simultaneously.

Hybrid B2B-plus-B2C infrastructure

Pre-owned electronics platform, Recommerce, combines three businesses in one entity. The company:

1) owns industrial refurbishment capacity (approximately 1.1 million devices a year through its own facilities in France and now Switzerland following the Verkaufen.ch acquisition in June 2025),

2) operates a B2B SaaS platform called CircularX that powers the white-label refurbishment and trade-in programmes for Vodafone, Orange and Bouygues Telecom, and

3) sells direct to consumers through its own storefront.

The model is capital-efficient because the carrier back-end business funds the operational infrastructure rather than requiring a separate consumer-marketing budget to acquire phones: Vodafone now refurbishes and resells 97% of its returned handsets through Recommerce. Recommerce has raised approximately $70 million in total, with the last priced equity round being a €50 million Series C in February 2018, and broke even at approximately €210 million of revenue in 2025.

Vertically-integrated Platforms

The vertically integrated, pre-owned smartphone model is best exemplified by Swappie. The company operates only with iPhones, buys devices directly from consumers, refurbishes in-house at owned facilities in Tallinn, Helsinki and in Germany, and sells direct to consumers through swappie.com.

The model is capital-intensive: Swappie has raised approximately $170 million of equity (the €108 million Series C in February 2022 led by Verdane being the largest round) plus €17 million of EIB venture debt in May 2024 directed specifically at refurbishment automation. The company was still loss-making with €248 million in revenues in 2024. The model gains a moat if the automation thesis flows through to unit-cost gains above those of an asset-light marketplace. The closest parallel is Carvana’s used car model in the US: capital-heavy, vertically integrated, loss-making for years before turning highly profitable on a structural unit-cost advantage at scale. Swappie is already active in 17 European markets.

For single European country ambitions, the capital requirement is materially smaller - perhaps $20 million to $50 million. Largo, a French refurbished-smartphone specialist with its own refurbishment facilities, IPO'd on Euronext Growth in April 2021 with €20 million of proceeds and now generates €34.82 million of revenue (FY24). AsGoodAsNew, a German vertically integrated refurbished-electronics player, has raised approximately $34.5 million in total and built refurbishment capacity of roughly 200,000 devices per year. Rebuy, another German player operating across refurbished smartphones, gaming, books and consumer electronics, has raised approximately $39.8 million in total and surpassed €220 million of revenue in 2024.

Horizontal classifieds and C2C platforms

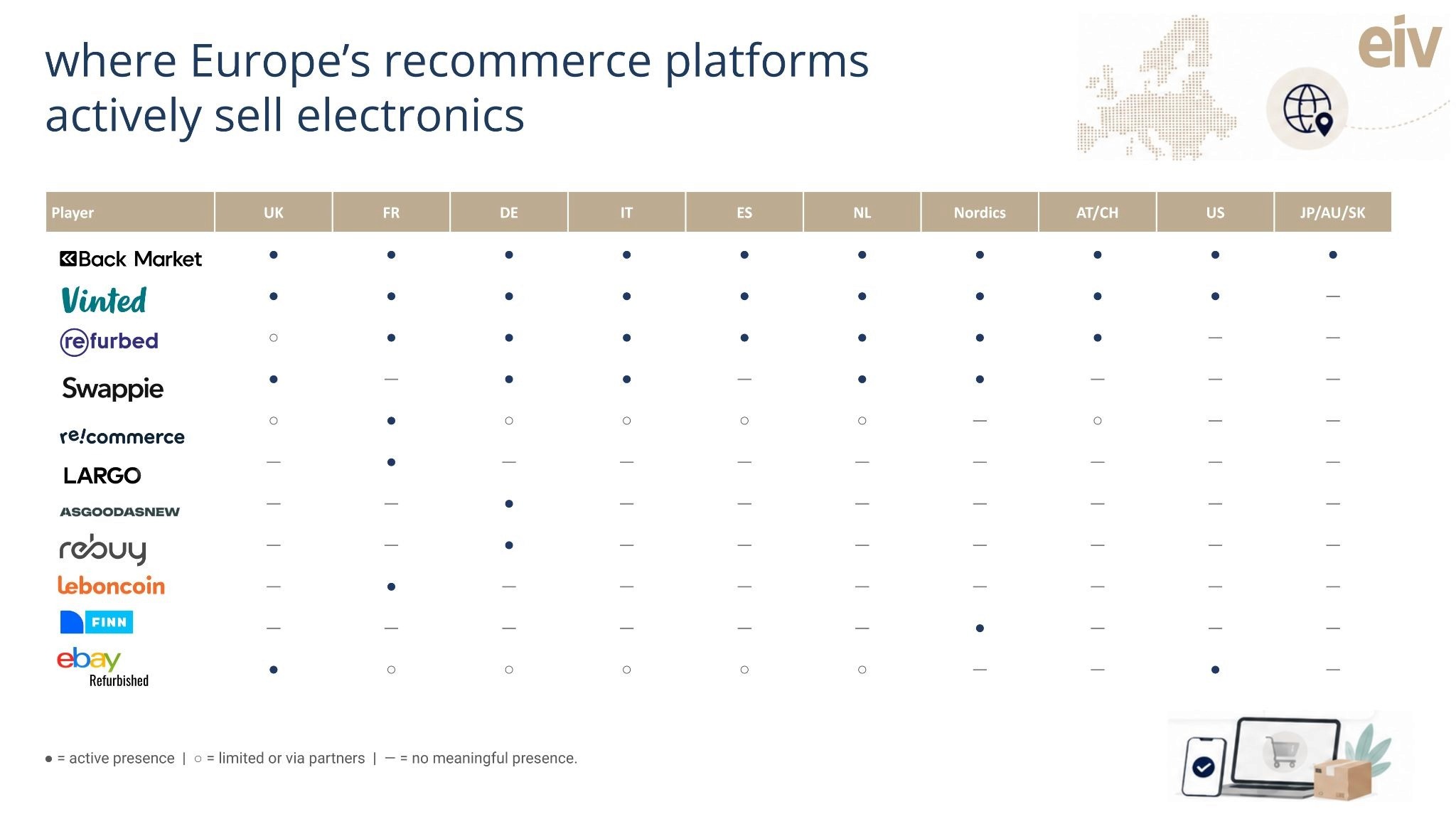

The fourth and final model is the horizontal classifieds and consumer-to-consumer platforms, which monetise listings rather than industrialising predictability. The European cohort includes Vinted (pan-European), Leboncoin (France), Kleinanzeigen (Germany), Wallapop (Spain), Marktplaats (Netherlands), Subito.it (Italy). We should add the two US platforms Facebook Marketplace (universal, particularly strong in the United Kingdom) and eBay.

None of them has yet built an industrial trust layer for electronics that approaches what the vertical specialists offer. Vinted's Electronics Verification Service is opt-in per item, with no warranty, no battery-health standard, and no certified-refurbisher onboarding.

Facebook Marketplace lacks buyer protection, with transactions completing as informal cash or peer-to-peer payment between strangers.

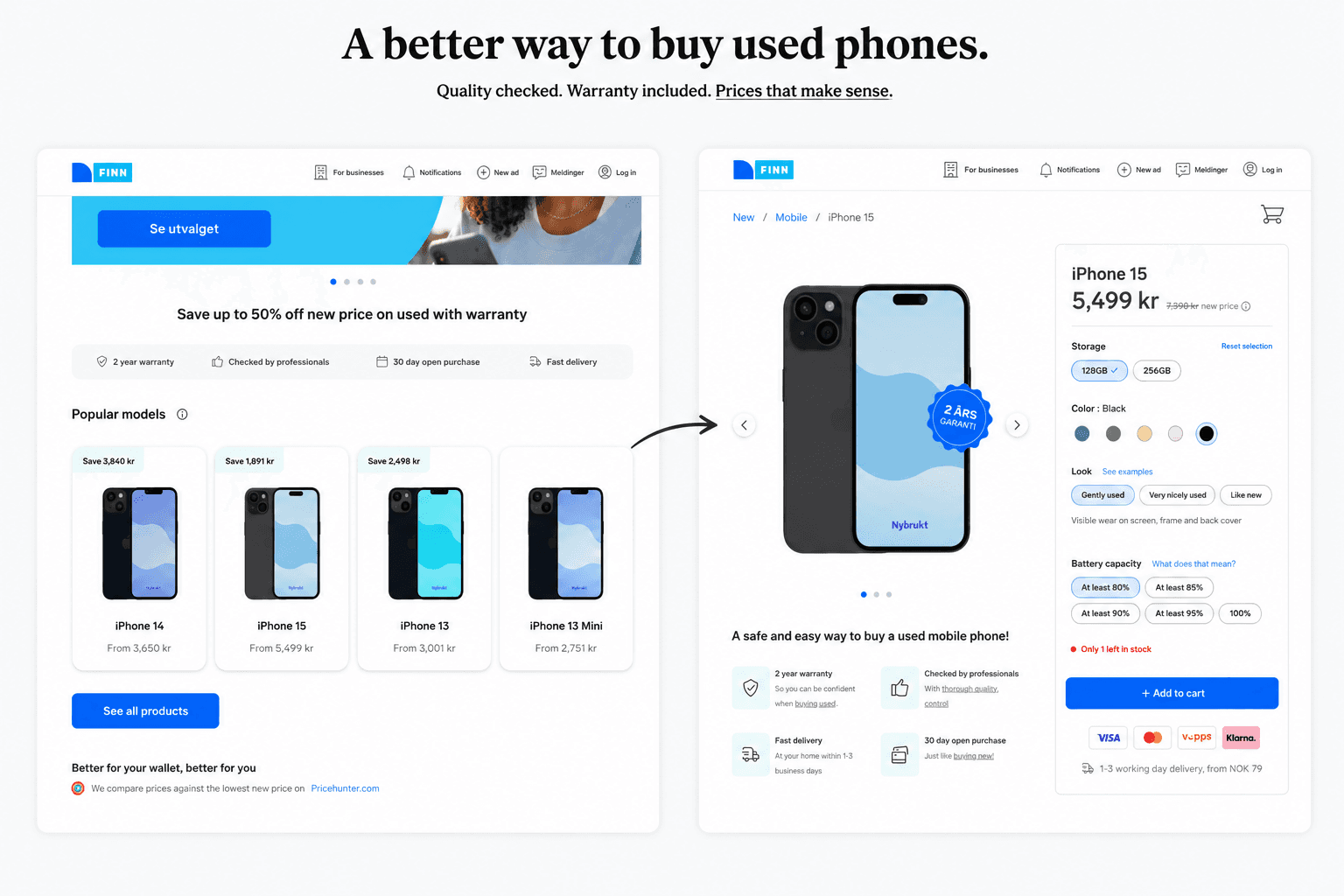

Perhaps the best implementation of a vertical-like user interface on a classifieds horizontal is to be found in Norway. Finn.no’s Nybrukt dedicated refurbished-phone storefront offers the buyer comparable simplicity and transparency to buying on Back Market, while outsourcing the actual inventory management and fulfillment to trusted third party professionals.

Why the verticals monetise better

The vertical specialists capture more revenue per transaction than the horizontals. A vertical electronics marketplace such as Back Market or Refurbed takes 10-15% of GMV as a transaction fee, plus a margin on the 12-month warranty it issues, a margin on the trade-in valuation when a consumer sends in an old device, and a fee per device on carrier and retailer partnerships.

A vertically-integrated player such as Swappie or AsGoodAsNew captures the full gross margin between the C2B intake price and the B2C resale price, plus warranty and protection products. A hybrid like Recommerce captures all of the above plus a recurring SaaS fee from the carrier programmes that run on CircularX.

By contrast, a horizontal classifieds platform such as Leboncoin or Vinted monetises only at the listing layer: a promoted placement, a buyer protection fee, or a small fixed percentage on payment and shipping. The vertical specialists exist because many consumers will pay a meaningful premium for trust, and the verticals are structurally positioned to capture that premium across multiple revenue lines.

Where the competitive pressure is coming from

The pressure on the vertical electronics specialists is coming from two directions, and both vary materially country by country.

OEM direct programmes at the premium tier

Apple has operated its certified-refurbished programme across Europe for years, with a one-year warranty and at a discount on retail. Samsung escalated the competition materially in January 2026 with the launch of Certified Re-Newed across the United Kingdom, France and Germany, selling refurbished Galaxy S25 devices directly. This matters most in France and Germany, where premium-device penetration is highest and where carrier trade-in ecosystems are already mature.

France illustrates the dynamic most clearly. At the front end, several storefronts compete for the French consumer: Back Market, Refurbed, Samsung's new Certified Re-Newed store, the Orange and Bouygues carrier programmes (via Recommerce), plus country specialists like Largo and CertiDeal.

Horizontal classifieds and C2C platforms, conditional and country-specific

Vinted has the overall scale to matter (€10.8 billion of group GMV across 26 markets in 2025), but its electronics-specific GMV is most probably an order of magnitude smaller than Back Market's. Becoming a real competitor in phones and laptops requires committing to industrial trust infrastructure (warranty backstops, certified-refurbisher onboarding, battery-health guarantees), which Vinted has not yet done beyond a per-item opt-in Electronics Verification Service.

The risk from horizontal classifieds is conditional and concentrated. It builds in markets where the horizontal already owns the consumer's reflex for buying used items generally: France via Leboncoin, Germany via Kleinanzeigen, Spain via Wallapop, the Netherlands via Marktplaats. In each of these the consumer base and listing infrastructure already exist; the missing piece is the trust layer that electronics specifically requires, and whether the platform owner invests in it is what turns the conditional risk into actual disruption. Finn.no in Norway is so far the only horizontal in Europe to have actually built this trust layer, via its Nybrukt dedicated refurbished-phone storefront launched in February 2023

Facebook Marketplace sits in the background across all markets as the free C2C option but lacks any verification or trust infrastructure, which keeps it a price-floor competitor rather than a strategic threat.

How will this play out?

The European electronics-recommerce market has matured substantially over the last three years. Back Market and Refurbed are entrenched at the top of the asset-light cohort with Recommerce dominant in B2B carrier infrastructure. The structural conditions today look different from the period when those companies were built: a new B2C aggregator launching at pan-European scale would need to fund a multi-year catch-up against incumbents who are now profitable and self-funded, which makes the economics structurally harder than they were in 2020 or 2022.

In today’s environment, the next phase of value creation is more likely to come from consolidation among existing players. The clearest example is Recommerce’s acquisition of Verkaufen.ch in Switzerland in June 2025. The deal strengthened Recommerce’s vertically integrated refurbishment infrastructure in Switzerland by adding 30 in-house technicians, Apple and Samsung certified-partner status, AI-powered device diagnostics, and forward trade-in technology.

The vertically integrated specialists are arguably already exit-ready - with mobile carrier groups, consumer-electronics retailers, horizontal C2C platforms and circular-economy-focused private equity the most natural acquirers.

Almost every European country has its own, vertically-integrated specialists: Largo, Smaaart, and CertiDeal in France, AsGoodAsNew and Rebuy in Germany, Reboxed in UK, TrenDevice in Italy, Metaphone in Spain, Revendo in Switzerland, Flip serving Romania and the wider CEE region, Nanowo and other domestic operators in Poland, Swappie at scale in the Nordics. Most operate at €30 million to €80 million of revenue with $20 million to $50 million of cumulative funding.

A closer look at the cap-table of these startups provides signals where consolidation is most likely to originate. Strategic horizontal ecommerce platforms are taking direct positions in the cohort: eMAG Ventures, the corporate-venture arm of eMAG (the dominant Romanian ecommerce platform) owns 42.26% of Flip in CEE; Sparrow Ventures, the venture arm of the Swiss retail incumbent Migros, backs Revendo; and telecom operators are also beginning to participate, with e& Capital backing Revibe in MENA.

The next phase of European electronics recommerce is unlikely to produce a single pan-European winner. Consumer behaviour, local classifieds strength, OEM programmes and country-level market structures are working against that outcome. But the market is still likely to consolidate as larger or better funded verticals seek to strengthen at the infrastructure layer: refurbishment capacity, reverse logistics, carrier integrations, certified supply networks and warranty operations increasingly benefit from scale. Cross border M&A in Europe is a given.

If you run or own a company active in this space, reach out to us. We would love to talk.